Welcome to IQ

Welcome to Isio’s latest quarterly pensions update for sponsors, summarising key events from the quarter and looking ahead to what’s coming up.

Change in funding positions since 31 December 2025

Commentary over the quarter

- The positions shown here are approximate using example portfolios based on market conditions as at 31 March 2026. There has been significant volatility in the market this quarter which we cover in more detail on the next tab. As a result your scheme’s position may differ from these examples depending on your scheme’s investments and events after the quarter end.

- Gilt yields have increased by over c.35 bps while corporate bonds have increased by c.60 bps.

- Inflation expectations have increased by c.30 bps over the quarter.

- Credit spreads have also increased at all durations.

- Assets were volatile over the quarter, but global equities ended the quarter down c.1%. In the examples shown here, asset values in both scenarios reduced over the quarter.

- We continue to see strong levels of insurer appetite, including further insurers launching propositions for smaller schemes. A competitive process is achievable for all but the very smallest schemes, where desired. Despite ongoing volatility, we have not seen an adverse impact on insurer pricing, which remains some of the best we have seen.

Is your scheme’s portfolio flexible enough to take advantage of market opportunities and can trustees act quickly enough to do so?

Background

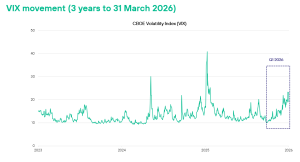

With geopolitical tensions escalating following U.S. military strikes on Iran, markets have once again entered a period of heightened uncertainty. Gilts, equities, and credit markets have reacted in a familiar pattern, with sentiment driven volatility dominating the short term. While price swings are uncomfortable, they are not unexpected. For long term investors such as pension schemes, they should not disrupt carefully considered strategies.

Isio’s view

In periods like this, maintaining focus on long term strategic asset allocation remains essential. For well-hedged schemes supported by robust collateral protection, market driven sell offs from the conflict can create opportunities to build towards target allocations.

The market response has been relatively contained: equity and bond moves have been moderate, though oil prices have risen sharply. In such conditions, making premature portfolio changes is rarely advantageous. Maintaining flexibility and monitoring developments closely can be the best way to add value. This is particularly true for corporate bonds and structured credit, where spreads remain tight and attractive entry points can be short‑lived.

This is an opportune moment for trustees to ensure their LDI hedging arrangements are robust. Recent gilt market volatility highlights the importance of reviewing collateral waterfalls, refreshing LDI design structures and, where appropriate, upgrading manager toolkits to ensure schemes remain well protected during sharp moves.

Why it matters

Periods of geopolitical volatility can be a real time stress test for asset allocation decisions, but they also create opportunity. Staying disciplined, maintaining liquidity, ensuring LDI resilience and being ready to act when dislocation presents value can help schemes accelerate progress toward long term objectives.

Salary Sacrifice update

Background

The 2025 Autumn Budget proposed that the tax-efficient pension contributions employers and employees can make through salary sacrifice arrangements will be capped from 2029.

Currently employers and employees benefit from reduced National Insurance Contributions (NIC) by redirecting portions of salary into pensions, as sacrificed pay is exempt from NIC (employer NIC = 15%). Under the new proposed rules, which are due to come into effect in 2029, only the first £2,000 sacrificed annually qualifies for NIC relief. These proposals would therefore increase NIC for both employers & employees under salary sacrifice arrangements.

Isio’s view

This is effectively a tax increase impacting both employers and employees. It will have a greater impact on higher earners and those that contribute more into pension via salary sacrifice.

It also reduces the effectiveness of pension saving, contrary to the government’s aims to encourage pension saving.

The House of Lords voted to make amendments to the legislation, but this was subsequently overturned by the government. There is lobbying against the proposal which may result in changes to the proposal between now and 2029. However, some form of salary sacrifice capping in future is still likely so employers should prepare now and consider reviewing their approach to salary or bonus sacrifice in advance of the changes.

Why it matters

Capping salary sacrifice will increase employer costs and create additional operational pressures. Proactive communication and financial planning will be key to protecting workforce well‑being and long‑term savings outcomes.

CMI 2025

Background

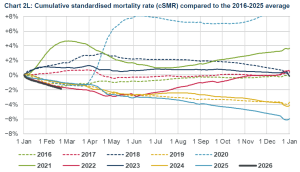

The Continuous Mortality Investigation (‘the CMI’) has updated its model on future longevity improvements.

The CMI 2025 model is largely a ‘business as usual’ update. There have been no changes in the methods used in the model this year, but the model has been updated for actual 2025 data.

Isio’s view

2025 was a record low year for UK mortality – following on from 2024’s experience of similarly low mortality (people are generally living longer). The recent positive experience since 2024 could signify a “new normal” or could reflect the expected result of mortality events in more vulnerable cohorts being brought forwards by the pandemic.

Added to this, wider global factors remain at play, strains and inflationary pressures on the economy are increasing, and the NHS funding and capacity issues appear not to be solved. Yet there are still potential tailwinds for life expectancies – e.g. the recent emergence of weight loss drugs.

This makes forecasting long-term trends based on this near-term data particularly challenging, coupled with the fact that trends in mortality continue to be different across different age groups.

Why it matters

The model is commonly used in actuarial valuations for multiple purposes, including cash funding and accounting.

Given the low mortality experience in 2025, and low mortality experience thus far in 2026, we have adjusted our best estimate life expectancies upwards compared to last year by 3 to 5 months, depending on age. We expect this to lead to around a 1% increase in best estimate liabilities, compared to the CMI 2024 model.

You can read more about this in our paper.

Looking forward to next quarter

- We’re excited to announce our 2026 Isio Conference, taking place on 9 September in London, “Disrupting complacency: Shaping a better future for pensions”. You can sign up for this event here. Investment managers can register here.

- The Pension Schemes Bill has now received Royal Assent. You can find a reminder of our post-Bill analysis here.

- To mark the launch of our 2026 Professional Independent Trustee Survey, we are hosting a webinar on 6 May. You can sign up for this event here.

-

Change in funding positions since 31 December 2025

Commentary over the quarter

- The positions shown here are approximate using example portfolios based on market conditions as at 31 March 2026. There has been significant volatility in the market this quarter which we cover in more detail on the next tab. As a result your scheme’s position may differ from these examples depending on your scheme’s investments and events after the quarter end.

- Gilt yields have increased by over c.35 bps while corporate bonds have increased by c.60 bps.

- Inflation expectations have increased by c.30 bps over the quarter.

- Credit spreads have also increased at all durations.

- Assets were volatile over the quarter, but global equities ended the quarter down c.1%. In the examples shown here, asset values in both scenarios reduced over the quarter.

- We continue to see strong levels of insurer appetite, including further insurers launching propositions for smaller schemes. A competitive process is achievable for all but the very smallest schemes, where desired. Despite ongoing volatility, we have not seen an adverse impact on insurer pricing, which remains some of the best we have seen.

-

Is your scheme’s portfolio flexible enough to take advantage of market opportunities and can trustees act quickly enough to do so?

Background

With geopolitical tensions escalating following U.S. military strikes on Iran, markets have once again entered a period of heightened uncertainty. Gilts, equities, and credit markets have reacted in a familiar pattern, with sentiment driven volatility dominating the short term. While price swings are uncomfortable, they are not unexpected. For long term investors such as pension schemes, they should not disrupt carefully considered strategies.Isio’s view

In periods like this, maintaining focus on long term strategic asset allocation remains essential. For well-hedged schemes supported by robust collateral protection, market driven sell offs from the conflict can create opportunities to build towards target allocations.

The market response has been relatively contained: equity and bond moves have been moderate, though oil prices have risen sharply. In such conditions, making premature portfolio changes is rarely advantageous. Maintaining flexibility and monitoring developments closely can be the best way to add value. This is particularly true for corporate bonds and structured credit, where spreads remain tight and attractive entry points can be short‑lived.

This is an opportune moment for trustees to ensure their LDI hedging arrangements are robust. Recent gilt market volatility highlights the importance of reviewing collateral waterfalls, refreshing LDI design structures and, where appropriate, upgrading manager toolkits to ensure schemes remain well protected during sharp moves.

Why it matters

Periods of geopolitical volatility can be a real time stress test for asset allocation decisions, but they also create opportunity. Staying disciplined, maintaining liquidity, ensuring LDI resilience and being ready to act when dislocation presents value can help schemes accelerate progress toward long term objectives. -

Salary Sacrifice update

Background

The 2025 Autumn Budget proposed that the tax-efficient pension contributions employers and employees can make through salary sacrifice arrangements will be capped from 2029.

Currently employers and employees benefit from reduced National Insurance Contributions (NIC) by redirecting portions of salary into pensions, as sacrificed pay is exempt from NIC (employer NIC = 15%). Under the new proposed rules, which are due to come into effect in 2029, only the first £2,000 sacrificed annually qualifies for NIC relief. These proposals would therefore increase NIC for both employers & employees under salary sacrifice arrangements.

Isio’s view

This is effectively a tax increase impacting both employers and employees. It will have a greater impact on higher earners and those that contribute more into pension via salary sacrifice.

It also reduces the effectiveness of pension saving, contrary to the government’s aims to encourage pension saving.

The House of Lords voted to make amendments to the legislation, but this was subsequently overturned by the government. There is lobbying against the proposal which may result in changes to the proposal between now and 2029. However, some form of salary sacrifice capping in future is still likely so employers should prepare now and consider reviewing their approach to salary or bonus sacrifice in advance of the changes.

Why it matters

Capping salary sacrifice will increase employer costs and create additional operational pressures. Proactive communication and financial planning will be key to protecting workforce well‑being and long‑term savings outcomes.

-

CMI 2025

Background

The Continuous Mortality Investigation (‘the CMI’) has updated its model on future longevity improvements.

The CMI 2025 model is largely a ‘business as usual’ update. There have been no changes in the methods used in the model this year, but the model has been updated for actual 2025 data.

Isio’s view

2025 was a record low year for UK mortality – following on from 2024’s experience of similarly low mortality (people are generally living longer). The recent positive experience since 2024 could signify a “new normal” or could reflect the expected result of mortality events in more vulnerable cohorts being brought forwards by the pandemic.

Added to this, wider global factors remain at play, strains and inflationary pressures on the economy are increasing, and the NHS funding and capacity issues appear not to be solved. Yet there are still potential tailwinds for life expectancies – e.g. the recent emergence of weight loss drugs.

This makes forecasting long-term trends based on this near-term data particularly challenging, coupled with the fact that trends in mortality continue to be different across different age groups.

Why it matters

The model is commonly used in actuarial valuations for multiple purposes, including cash funding and accounting.

Given the low mortality experience in 2025, and low mortality experience thus far in 2026, we have adjusted our best estimate life expectancies upwards compared to last year by 3 to 5 months, depending on age. We expect this to lead to around a 1% increase in best estimate liabilities, compared to the CMI 2024 model.

You can read more about this in our paper.

-

Looking forward to next quarter

- We’re excited to announce our 2026 Isio Conference, taking place on 9 September in London, “Disrupting complacency: Shaping a better future for pensions”. You can sign up for this event here. Investment managers can register here.

- The Pension Schemes Bill has now received Royal Assent. You can find a reminder of our post-Bill analysis here.

- To mark the launch of our 2026 Professional Independent Trustee Survey, we are hosting a webinar on 6 May. You can sign up for this event here.

Your opportunity to provide feedback on IQ

It has been one year since we launched IQ with the purpose of sharing a quarterly reflective analysis and forward look ahead. We would appreciate a couple of minutes of your time to complete this anonymous short survey to help us ensure we maximise the value of IQ for our readers.

Join our mailing list

Get the next issue of Isio Quarterly delivered straight to your inbox