Welcome to IQ

Welcome to Isio’s latest quarterly pensions update for sponsors, summarising key events from the quarter and looking ahead to what’s coming up.

Change since 30 September 2024

Commentary over the quarter

- Gilt yields have risen materially, by c. 55-60 basis points over the quarter while long-term inflation expectations have only risen by c. 5 basis points

- Global equity markets were up by c. 6% over the quarter

- These movements are likely to have a positive impact on funding levels for those schemes who aren’t fully hedged on their funding measures – as reductions in funding liabilities are likely to exceed corresponding falls in their LDI assets

- Credit spreads reduced by c. 10-15 basis points over the quarter – and thus accounting positions may have worsened for most schemes, other than those with lower hedging levels

- Anticipated insurer discount rates are up by c. 50 bps over the quarter, slightly lower than the movement in gilt yields. This should result in improvements for most schemes, other than those with higher levels of hedging where the gilt yield movement result in asset losses which exceed any reductions in estimated buyout liabilities

Commentary on accounting movements over the year

-

- Credit spreads reduced slightly over 2024 (c. 5-10 basis points), while global equity markets were up c. 20% over this period, and gilt yields increased significantly (c 100 basis points)

- This means that less well hedged (< c. 90%) schemes are expected to see improvements in their net balance sheet positions over the year

- In contrast schemes with higher hedging levels may see a worsening in net balance sheet positions due to the lower credit spreads, less (or no) equity exposure and potentially no cash contributions being paid by the sponsor

Recent market volatility

Background

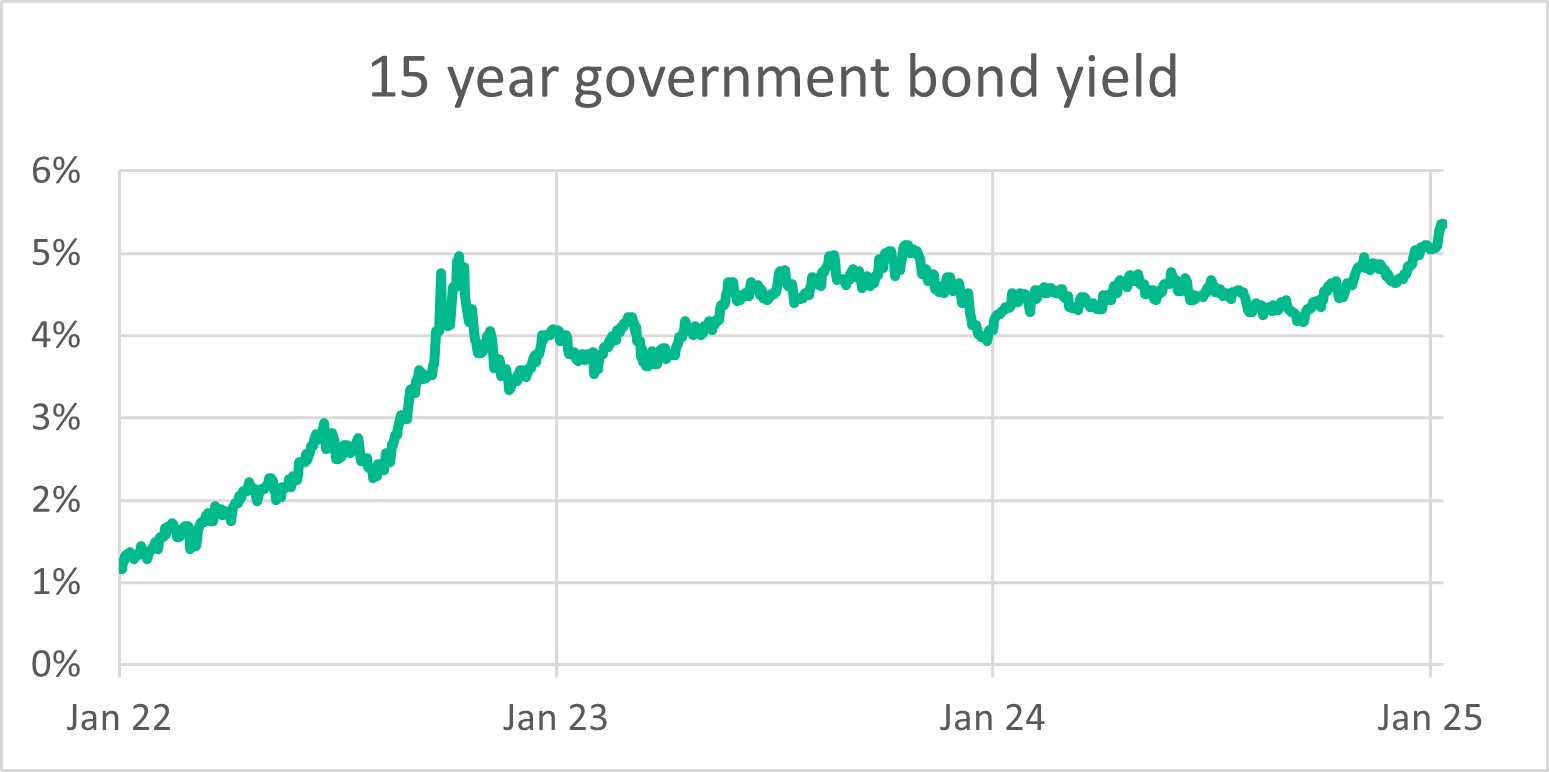

With the Government’s first Budget in late October 2024 and the US election in early November, we saw a lot of market uncertainty in Q4. Traditional growth assets performed well over 2024 while government bond yields have gradually been increasing over the year. In recent weeks gilt yields have exceeded the levels at the peak of the Autumn 2022 LDI crisis and achieving yields not seen since before the 2008 Credit Crunch.

Isio’s view

Given the 2022 LDI crisis, there has been understandable concern at the recent rise in yields. The key difference this time around is the speed of change. During the LDI crisis, yields moved by more than 50 basis points in a single day. In contrast, we’re now seeing changes of 50 basis points over months, rather than days (see graphic).

DB pension schemes now also generally have greater collateral buffers, lower leverage levels and better collateral management strategies in place to cope with yield rises.

Rising yields and the performance of growth assets over 2024 will generally have a positive impact on the funding positions for a typical UK DB Scheme. It will be important to understand the scale of this impact on your Scheme and whether any gains could be locked in.

Why it matters

While we expect pension trustees to be actively managing the situation, we recommend that pension scheme sponsors:

- Confirm whether collateral buffers remain sufficient in size and liquidity;

- Assess the impact on your schemes’ funding positions;

- Consider whether now is the right time to lock in some of these funding gains, e.g. by increasing hedging levels, de-risking assets etc.; and

- Consider whether scheme factors are excessively generous, in current market conditions.

Views on TPR’s updated covenant guidance

Background

The Pensions Regulator issued its detailed guidance on assessing covenant in December, to accompany the new Funding Code. There is plenty to digest in over 150 pages of guidance, but the fundamental principle – that employer covenant is the financial ability of entities with a legal obligation to support a pension scheme – remains the same. The primary areas of focus are assessing the cash generation of the employer (as well as any contingent assets) and understanding the employer’s future outlook or its ‘Prospects’.

Isio’s view

The guidance provides more detail on how to assess the new subjective covenant metrics of:

- Covenant Longevity period – how long the employer will be able to support the scheme;

- Covenant Reliability period – the period over which the trustee has reasonable certainty over cash generated by the employer;

- Reasonable affordability – the contributions the employer can reasonably afford;

- Maximum Affordable Contributions – the cash that might be available to be paid to the scheme to remedy any deficit from a downside scheme stress event.

The consequences of a cautious assessment by the trustees will be a shorter period for generation of scheme asset returns, and therefore increased cash required from the employer. TPR’s previous guidance wanted trustees to behave like bankers, but treating trustees like investors and articulating the value story and outlook for the employer will now result in a better outcome for sponsors.

Why it matters

If employers are passive in the covenant assessment, it is likely to result in Trustees wanting more cash than necessary.

Employers taking the initiative with trustees and providing information which easily translates into these new covenant concepts will help achieve the best outcomes.

For more detail on the new covenant guidance, please read our summary below.

Read more about TPR’s New Covenant GuidanceThe latest Clara deal, and what more may be to come

Background

Clara-Pensions announced their third deal at the end of 2024 – taking on the benefits of the c.1,500 members of the Wates Pension Fund. The Wates transaction is valued at c.£210m – with an additional £19m provided by the sponsor and further capital security provided by Clara. The Wates members join the existing 20,000 members within Clara and £1.2bn of assets under management.

Isio’s view

This is a milestone deal for Clara – their first with an active sponsor – and proof of concept that member outcomes can be improved by a superfund transaction despite giving up an ongoing sponsor covenant. The fact they can deal with illiquid assets in-specie could also open the risk-settlement door to a wider range of schemes.

More deals are in the pipeline, and we understand that Clara are continuing to look towards innovation in this space including: options for the strongest sponsors to participate via contingent guarantees; options for co-investment for sponsors who wish to share in investment upsides; and options for PPF rescue at less than 100% of benefits (but more than PPF benefits). Clearly more “vanilla” deals are essential to continue to establish the model but it would be great to see more innovation in this area.

Why it matters

For sponsors this is another pathway to de-risking your balance sheet and mitigating future cash calls from mostly legacy defined benefit arrangements. For schemes that are really well funded insurance or run-on solutions may still be the only game in town. However, for those that are a bit further away, the opportunity to settle your liabilities is now closer than ever.

Increases in National Insurance and the National Minimum/Living Wage

Background

The recent increase to employer National Insurance (NI) was widely billed in advance of the Autumn Budget, yet the scale of the changes came as a surprise – in particular the lowering of the Secondary Threshold, which will likely have a bigger impact on the amount of NI paid by businesses than the increase in the headline rate.

Another change was the increase in the National Minimum/Living Wage. For individuals aged 21 and over this will increase by almost 7%, whereas for individuals aged 18 – 20 there will be an even larger increase of 16%.

Isio’s view

Rebalancing reward away from pay and into other benefits that do not attract employer NI can help to manage costs.

Directing more reward into pensions is one obvious way of doing this, through core pension contributions, as well as bonus sacrifice and/or a shared cost Additional Voluntary Contribution (AVC).

Equally, those businesses already using existing salary sacrifice arrangements (and sharing some of the NI savings in the form of employee contributions), will need to consider whether these need to be revisited in light of the higher savings.

Also worth considering are approved non-financial salary sacrifice arrangements such as electric vehicles, cycle to work and technology schemes.

Why it matters

The increase in employer’s NI rate alongside the reduction in the threshold coupled with the increases in minimum wage could mean employers are likely to be facing a very significant increase in their employment costs. The cost of employing an individual earning National Minimum Wage, for example, could increase by over 10% of payroll.

For more commentary on the Budget changes, see our Insights page here.

What the Budget and Employment Rights Bill mean for payrollWhat to watch out for in 2025

Background

Investment returns over 2024 resulted in another great year for DB pension scheme funding levels, both for the corporate sector and, in particular, the public sector, many of which have accelerated their journey plans.

2025 brings a new economic and political landscape with equity markets at all-time highs but heavily concentrated, credit spreads being historically tight and long-term gilt yields at levels not seen for almost 20 years.

Isio’s view

We believe now is the time to reassess investment strategy and asset allocation. Our themes for 2025 are:

- Reallocating profits from expensive growth assets into fresh opportunities;

- Keeping dry powder waiting for a better environment to deploy risk;

- Tackling structural challenges facing pension scheme investors

Why it matters

Looking forward there are challenges facing risk assets that are priced for perfection based on their high Price / Earnings ratios and tight credit spreads. With many DB schemes ahead of journey plan, now is time to reassess the asset allocation to ensure the balance is right.

- The PPF initially consulted in the autumn on maintaining the levy at £100m for 2025/26, but has confirmed it will delay publishing the outcome until the end of January to engage with the Department of Work and Pensions – providing optimism that legislative change to facilitate nil levies may be forthcoming.

- A consultation on the next version of the CMI longevity projection model is due to be issued in February 2025, with the model itself released in Q2. This update may represent a significant overhaul of the model compared to previous versions.

- Isio has released a comprehensive analysis on the state of the Gender Pay Gap in the UK. Pay gap reporting obligations are expanding and the report also provides insights on how employers can prepare for the forthcoming changes. Download your copy here.

- As employers work through 31 December financial statements, auditors are increasingly pressing for investigations into Virgin Media issues. We’ve been exploring this topic with the Big 4 auditors, and will be releasing an Insights article soon. If you want to be notified when this is released, please subscribe below.

-

Change since 30 September 2024

Commentary over the quarter

- Gilt yields have risen materially, by c. 55-60 basis points over the quarter while long-term inflation expectations have only risen by c. 5 basis points

- Global equity markets were up by c. 6% over the quarter

- These movements are likely to have a positive impact on funding levels for those schemes who aren’t fully hedged on their funding measures – as reductions in funding liabilities are likely to exceed corresponding falls in their LDI assets

- Credit spreads reduced by c. 10-15 basis points over the quarter – and thus accounting positions may have worsened for most schemes, other than those with lower hedging levels

- Anticipated insurer discount rates are up by c. 50 bps over the quarter, slightly lower than the movement in gilt yields. This should result in improvements for most schemes, other than those with higher levels of hedging where the gilt yield movement result in asset losses which exceed any reductions in estimated buyout liabilities

Commentary on accounting movements over the year

-

- Credit spreads reduced slightly over 2024 (c. 5-10 basis points), while global equity markets were up c. 20% over this period, and gilt yields increased significantly (c 100 basis points)

- This means that less well hedged (< c. 90%) schemes are expected to see improvements in their net balance sheet positions over the year

- In contrast schemes with higher hedging levels may see a worsening in net balance sheet positions due to the lower credit spreads, less (or no) equity exposure and potentially no cash contributions being paid by the sponsor

-

Recent market volatility

Background

With the Government’s first Budget in late October 2024 and the US election in early November, we saw a lot of market uncertainty in Q4. Traditional growth assets performed well over 2024 while government bond yields have gradually been increasing over the year. In recent weeks gilt yields have exceeded the levels at the peak of the Autumn 2022 LDI crisis and achieving yields not seen since before the 2008 Credit Crunch.

Isio’s view

Given the 2022 LDI crisis, there has been understandable concern at the recent rise in yields. The key difference this time around is the speed of change. During the LDI crisis, yields moved by more than 50 basis points in a single day. In contrast, we’re now seeing changes of 50 basis points over months, rather than days (see graphic).

DB pension schemes now also generally have greater collateral buffers, lower leverage levels and better collateral management strategies in place to cope with yield rises.

Rising yields and the performance of growth assets over 2024 will generally have a positive impact on the funding positions for a typical UK DB Scheme. It will be important to understand the scale of this impact on your Scheme and whether any gains could be locked in.

Why it matters

While we expect pension trustees to be actively managing the situation, we recommend that pension scheme sponsors:

- Confirm whether collateral buffers remain sufficient in size and liquidity;

- Assess the impact on your schemes’ funding positions;

- Consider whether now is the right time to lock in some of these funding gains, e.g. by increasing hedging levels, de-risking assets etc.; and

- Consider whether scheme factors are excessively generous, in current market conditions.

-

Views on TPR’s updated covenant guidance

Background

The Pensions Regulator issued its detailed guidance on assessing covenant in December, to accompany the new Funding Code. There is plenty to digest in over 150 pages of guidance, but the fundamental principle – that employer covenant is the financial ability of entities with a legal obligation to support a pension scheme – remains the same. The primary areas of focus are assessing the cash generation of the employer (as well as any contingent assets) and understanding the employer’s future outlook or its ‘Prospects’.

Isio’s view

The guidance provides more detail on how to assess the new subjective covenant metrics of:

- Covenant Longevity period – how long the employer will be able to support the scheme;

- Covenant Reliability period – the period over which the trustee has reasonable certainty over cash generated by the employer;

- Reasonable affordability – the contributions the employer can reasonably afford;

- Maximum Affordable Contributions – the cash that might be available to be paid to the scheme to remedy any deficit from a downside scheme stress event.

The consequences of a cautious assessment by the trustees will be a shorter period for generation of scheme asset returns, and therefore increased cash required from the employer. TPR’s previous guidance wanted trustees to behave like bankers, but treating trustees like investors and articulating the value story and outlook for the employer will now result in a better outcome for sponsors.

Why it matters

If employers are passive in the covenant assessment, it is likely to result in Trustees wanting more cash than necessary.

Employers taking the initiative with trustees and providing information which easily translates into these new covenant concepts will help achieve the best outcomes.

For more detail on the new covenant guidance, please read our summary below.

Read more about TPR’s New Covenant Guidance -

The latest Clara deal, and what more may be to come

Background

Clara-Pensions announced their third deal at the end of 2024 – taking on the benefits of the c.1,500 members of the Wates Pension Fund. The Wates transaction is valued at c.£210m – with an additional £19m provided by the sponsor and further capital security provided by Clara. The Wates members join the existing 20,000 members within Clara and £1.2bn of assets under management.

Isio’s view

This is a milestone deal for Clara – their first with an active sponsor – and proof of concept that member outcomes can be improved by a superfund transaction despite giving up an ongoing sponsor covenant. The fact they can deal with illiquid assets in-specie could also open the risk-settlement door to a wider range of schemes.

More deals are in the pipeline, and we understand that Clara are continuing to look towards innovation in this space including: options for the strongest sponsors to participate via contingent guarantees; options for co-investment for sponsors who wish to share in investment upsides; and options for PPF rescue at less than 100% of benefits (but more than PPF benefits). Clearly more “vanilla” deals are essential to continue to establish the model but it would be great to see more innovation in this area.

Why it matters

For sponsors this is another pathway to de-risking your balance sheet and mitigating future cash calls from mostly legacy defined benefit arrangements. For schemes that are really well funded insurance or run-on solutions may still be the only game in town. However, for those that are a bit further away, the opportunity to settle your liabilities is now closer than ever.

-

Increases in National Insurance and the National Minimum/Living Wage

Background

The recent increase to employer National Insurance (NI) was widely billed in advance of the Autumn Budget, yet the scale of the changes came as a surprise – in particular the lowering of the Secondary Threshold, which will likely have a bigger impact on the amount of NI paid by businesses than the increase in the headline rate.

Another change was the increase in the National Minimum/Living Wage. For individuals aged 21 and over this will increase by almost 7%, whereas for individuals aged 18 – 20 there will be an even larger increase of 16%.

Isio’s view

Rebalancing reward away from pay and into other benefits that do not attract employer NI can help to manage costs.

Directing more reward into pensions is one obvious way of doing this, through core pension contributions, as well as bonus sacrifice and/or a shared cost Additional Voluntary Contribution (AVC).

Equally, those businesses already using existing salary sacrifice arrangements (and sharing some of the NI savings in the form of employee contributions), will need to consider whether these need to be revisited in light of the higher savings.

Also worth considering are approved non-financial salary sacrifice arrangements such as electric vehicles, cycle to work and technology schemes.

Why it matters

The increase in employer’s NI rate alongside the reduction in the threshold coupled with the increases in minimum wage could mean employers are likely to be facing a very significant increase in their employment costs. The cost of employing an individual earning National Minimum Wage, for example, could increase by over 10% of payroll.

For more commentary on the Budget changes, see our Insights page here.

What the Budget and Employment Rights Bill mean for payroll -

What to watch out for in 2025

Background

Investment returns over 2024 resulted in another great year for DB pension scheme funding levels, both for the corporate sector and, in particular, the public sector, many of which have accelerated their journey plans.

2025 brings a new economic and political landscape with equity markets at all-time highs but heavily concentrated, credit spreads being historically tight and long-term gilt yields at levels not seen for almost 20 years.

Isio’s view

We believe now is the time to reassess investment strategy and asset allocation. Our themes for 2025 are:

- Reallocating profits from expensive growth assets into fresh opportunities;

- Keeping dry powder waiting for a better environment to deploy risk;

- Tackling structural challenges facing pension scheme investors

Why it matters

Read the full commentary

Looking forward there are challenges facing risk assets that are priced for perfection based on their high Price / Earnings ratios and tight credit spreads. With many DB schemes ahead of journey plan, now is time to reassess the asset allocation to ensure the balance is right. -

- The PPF initially consulted in the autumn on maintaining the levy at £100m for 2025/26, but has confirmed it will delay publishing the outcome until the end of January to engage with the Department of Work and Pensions – providing optimism that legislative change to facilitate nil levies may be forthcoming.

- A consultation on the next version of the CMI longevity projection model is due to be issued in February 2025, with the model itself released in Q2. This update may represent a significant overhaul of the model compared to previous versions.

- Isio has released a comprehensive analysis on the state of the Gender Pay Gap in the UK. Pay gap reporting obligations are expanding and the report also provides insights on how employers can prepare for the forthcoming changes. Download your copy here.

- As employers work through 31 December financial statements, auditors are increasingly pressing for investigations into Virgin Media issues. We’ve been exploring this topic with the Big 4 auditors, and will be releasing an Insights article soon. If you want to be notified when this is released, please subscribe below.

Join our mailing list

Get the next issue of Isio Quarterly delivered straight to your inbox