Welcome to IQ

Welcome to Isio’s latest quarterly pensions update for sponsors, summarising key events from the quarter and looking ahead to what’s coming up.

Changes since 30 June 2025

Commentary over the quarter

- Gilt yields have increased by c. 25 basis points.

- Inflation expectations are broadly unchanged.

- Credit spreads have narrowed by c. 2 basis points at most durations, which we expect will have a negligible impact on accounting positions.

- Global equity markets were up by c. 9-10% over Q3 2025, driving funding improvements.

- Insurer appetite continues to be strong going into Q4 – albeit demand may vary depending on the insurer and whether they have already filled their pipeline or not.

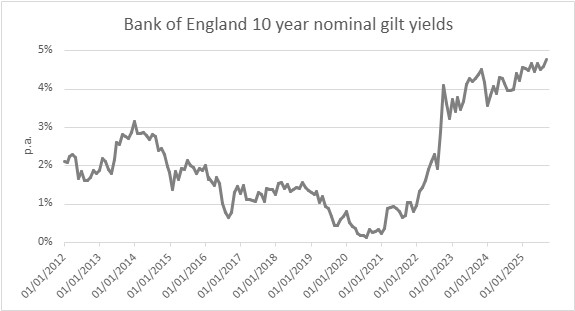

Gilt yields rose sharply over 2022 and have remained high since then (see graph below). This has several implications which sponsors of DB schemes should make sure they raise with their trustees.

Check when trustees last reviewed factors and ask for the next planned review to be brought forward where necessary.

If your scheme’s actuarial factors were set when gilt yields were lower, they may be too generous now. This could lead to a funding strain when members choose certain options, such as taking a cash lump sum at retirement or retiring early.

Reassess DB strategies and engage with trustees on implementation.

Liabilities have reduced by around a third since early 2022 for a typical DB scheme. Many sponsors have grown over the same period, potentially making new options available, for example, targeting risk settlement or gradual surplus release.

Engage with trustees to review hedging levels and consider segregated LDI if possible.

Whilst some speculate that gilt yields will revert to the lower levels seen before 2022, all major bond markets are under pressure from growing government debt levels. Given the uncertainty, we expect that fully hedged schemes will remain so and trustees and sponsors of underhedged schemes may seek to lock in gains by hedging more now. LDI arrangements have changed to avoid a repeat of 2022, but arguably for pooled LDI investors the changes protect the counterparties, with schemes being exposed to the same liquidity risks if they need to act quickly.

Background

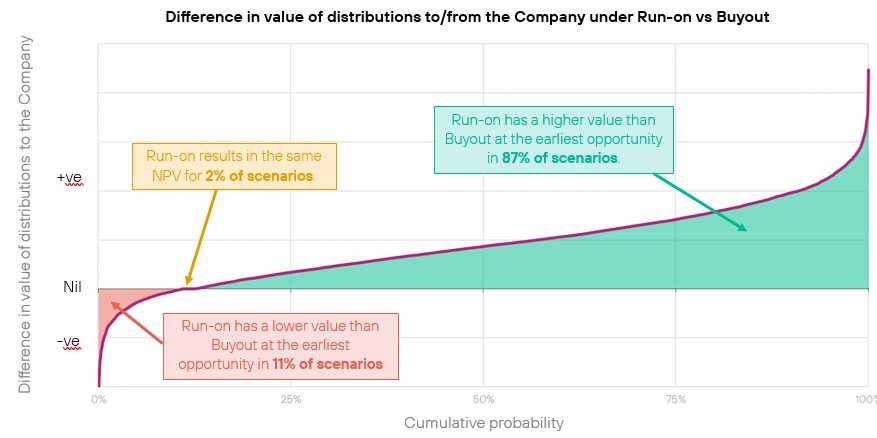

Releasing surplus to sponsors will become easier from late 2027, meaning that some DB schemes will become an opportunity to create value for sponsors. Running on could unlock material value, but this needs to be carefully weighed against downside risks. TPR have recently released guidance on this subject.

Isio’s view

The risk-reward trade-offs are nuanced, and traditional deterministic projections give insufficient insight to make informed decisions. Modern stochastic modelling techniques can help sponsors and trustees be more sophisticated in evaluating options, for example, how likely is it that a sponsor will regret running on, rather than insuring their scheme at the earliest opportunity? We’ve developed a cost-effective way of using this type of modern analysis to help schemes and sponsors properly quantify their options – see the graph for an example of the output this can produce. So far, we’ve helped over 20 schemes with assets from £50m to £5 billion, and more information is available here.

Why it matters

Many schemes are at inflection points and trustees are looking for sponsors to set out their preferred strategy. Stakeholder views can vary widely between and within organisations, and corporate boards should be provided with the insight needed to make informed decisions.

Background

The DB Funding Code has now been in effect for a year and the first tranche of scheme valuations will be due by the end of 2025. Our recent funding survey of around 350 Isio clients gives insight to the direction of travel and key areas of focus.

Isio’s view

Some interesting statistics from our survey include:

- 61% of schemes surveyed were already in a surplus at their most recent valuation. The average scheme has then seen a 13% improvement in funding levels over the last three years.

- 53% of schemes expect to adopt Fast Track to comply with the new requirements, whilst 11% expect to go the Bespoke route and 36% of schemes are still unsure.

- Larger schemes are more inclined to target run on in the long term whereas smaller schemes remain focussed on insurance buyout.

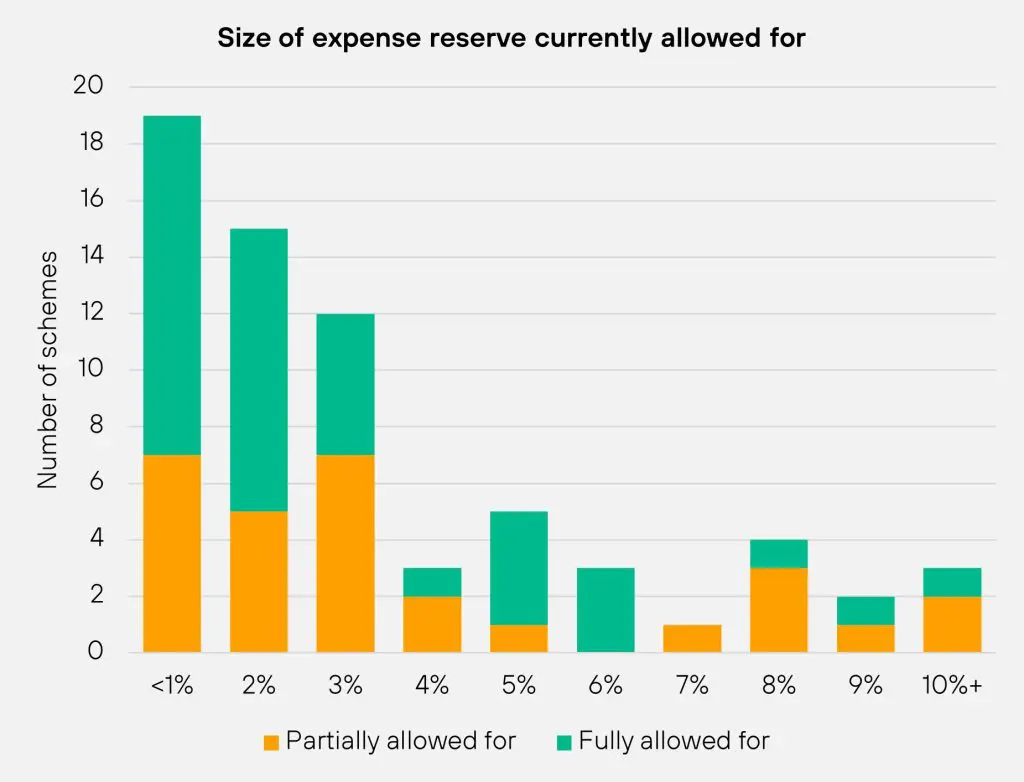

- Larger schemes are also more likely to have an existing expense reserve than smaller schemes. For those schemes adopting a reserve, we’ve seen a wide range which can either fully or partially cover expenses (see graph). Making allowance for expenses is expected to increase under the new regime.

Why it matters

Companies should be actively engaging with their trustees on the first valuations under the new Funding Code.

In particular, companies should:

- Make sure that the long-term objective is aligned to their strategic goals and doesn’t create any unnecessary cash risk.

- Engage early with Trustees on future use of surplus.

- Actively consider the Fast Track and Bespoke regulatory compliance routes.

- Diligently review expense reserve allowances.

Don’t assume that a surplus means no company input is required. Please email your Isio contact if you would like a copy of the full funding survey report.

Background

The government is making two helpful changes to the Pension Schemes Bill:

- The first change will allow Scheme Actuaries to provide a new confirmation for historic changes to the scheme, where actuarial certification is either missing or wasn’t recorded properly, helping resolve the Virgin Media issue.

- The second change, expected in the next round of amendments to the bill, will remove the PPF admin levy, which follows the PPF’s announcement that it will not be charging the main PPF levy for this year (2025/26).

Isio’s view

Being able to provide an actuarial confirmation will help the industry to resolve the headache caused by missing or incomplete scheme documentation. Sensible legal and actuarial advice is needed to navigate this issue and some exceptions will apply. The move to a zero PPF levy this year and removing the PPF admin levy are positive steps. However, the PPF levy is not guaranteed to be zero in future.

Why it matters

Virgin Media issues have been causing headaches for accounting disclosures and risk settlement transactions since the ruling in 2023. The new changes largely help to resolve this issue, but do need to be worked through with the Trustee and Scheme Actuary.

The PPF’s funding position is in rude health. Removing high levy payments and the admin around them is positive for sponsors and trustees and gives a P&L benefit for sponsors, although this does not mean the PPF levies are gone for good.

Looking forward to next quarter

- We will be hosting a breakfast event at the London Stock Exchange with David Smith as the guest speaker and an expert panel including DWP director Kerstin Parker on 17 November. This event is for senior finance leaders with responsibility for their organisation’s DB and DC schemes. Register here.

- On 18 November, we will be hosting our Fiduciary Management Conference Live event on Zoom. Learn more and register here.

- Keep an eye out for an email about our upcoming accounting webinar.

- The Chancellor is expected to announce her Autumn budget on Wednesday 26 November. The press has speculated on the inclusion of several pensions related topics. We will be listening carefully to the content on Budget day and will let you know any implications in the next edition of IQ.

-

Changes since 30 June 2025

Commentary over the quarter

- Gilt yields have increased by c. 25 basis points.

- Inflation expectations are broadly unchanged.

- Credit spreads have narrowed by c. 2 basis points at most durations, which we expect will have a negligible impact on accounting positions.

- Global equity markets were up by c. 9-10% over Q3 2025, driving funding improvements.

- Insurer appetite continues to be strong going into Q4 – albeit demand may vary depending on the insurer and whether they have already filled their pipeline or not.

-

Gilt yields rose sharply over 2022 and have remained high since then (see graph below). This has several implications which sponsors of DB schemes should make sure they raise with their trustees.

Check when trustees last reviewed factors and ask for the next planned review to be brought forward where necessary.

If your scheme’s actuarial factors were set when gilt yields were lower, they may be too generous now. This could lead to a funding strain when members choose certain options, such as taking a cash lump sum at retirement or retiring early.

Reassess DB strategies and engage with trustees on implementation.

Liabilities have reduced by around a third since early 2022 for a typical DB scheme. Many sponsors have grown over the same period, potentially making new options available, for example, targeting risk settlement or gradual surplus release.

Engage with trustees to review hedging levels and consider segregated LDI if possible.

Whilst some speculate that gilt yields will revert to the lower levels seen before 2022, all major bond markets are under pressure from growing government debt levels. Given the uncertainty, we expect that fully hedged schemes will remain so and trustees and sponsors of underhedged schemes may seek to lock in gains by hedging more now. LDI arrangements have changed to avoid a repeat of 2022, but arguably for pooled LDI investors the changes protect the counterparties, with schemes being exposed to the same liquidity risks if they need to act quickly.

-

Background

Releasing surplus to sponsors will become easier from late 2027, meaning that some DB schemes will become an opportunity to create value for sponsors. Running on could unlock material value, but this needs to be carefully weighed against downside risks. TPR have recently released guidance on this subject.

Isio’s view

The risk-reward trade-offs are nuanced, and traditional deterministic projections give insufficient insight to make informed decisions. Modern stochastic modelling techniques can help sponsors and trustees be more sophisticated in evaluating options, for example, how likely is it that a sponsor will regret running on, rather than insuring their scheme at the earliest opportunity? We’ve developed a cost-effective way of using this type of modern analysis to help schemes and sponsors properly quantify their options – see the graph for an example of the output this can produce. So far, we’ve helped over 20 schemes with assets from £50m to £5 billion, and more information is available here.

Why it matters

Many schemes are at inflection points and trustees are looking for sponsors to set out their preferred strategy. Stakeholder views can vary widely between and within organisations, and corporate boards should be provided with the insight needed to make informed decisions.

-

Background

The DB Funding Code has now been in effect for a year and the first tranche of scheme valuations will be due by the end of 2025. Our recent funding survey of around 350 Isio clients gives insight to the direction of travel and key areas of focus.

Isio’s view

Some interesting statistics from our survey include:

- 61% of schemes surveyed were already in a surplus at their most recent valuation. The average scheme has then seen a 13% improvement in funding levels over the last three years.

- 53% of schemes expect to adopt Fast Track to comply with the new requirements, whilst 11% expect to go the Bespoke route and 36% of schemes are still unsure.

- Larger schemes are more inclined to target run on in the long term whereas smaller schemes remain focussed on insurance buyout.

- Larger schemes are also more likely to have an existing expense reserve than smaller schemes. For those schemes adopting a reserve, we’ve seen a wide range which can either fully or partially cover expenses (see graph). Making allowance for expenses is expected to increase under the new regime.

Why it matters

Companies should be actively engaging with their trustees on the first valuations under the new Funding Code.

In particular, companies should:

- Make sure that the long-term objective is aligned to their strategic goals and doesn’t create any unnecessary cash risk.

- Engage early with Trustees on future use of surplus.

- Actively consider the Fast Track and Bespoke regulatory compliance routes.

- Diligently review expense reserve allowances.

Don’t assume that a surplus means no company input is required. Please email your Isio contact if you would like a copy of the full funding survey report.

-

Background

The government is making two helpful changes to the Pension Schemes Bill:

- The first change will allow Scheme Actuaries to provide a new confirmation for historic changes to the scheme, where actuarial certification is either missing or wasn’t recorded properly, helping resolve the Virgin Media issue.

- The second change, expected in the next round of amendments to the bill, will remove the PPF admin levy, which follows the PPF’s announcement that it will not be charging the main PPF levy for this year (2025/26).

Isio’s view

Being able to provide an actuarial confirmation will help the industry to resolve the headache caused by missing or incomplete scheme documentation. Sensible legal and actuarial advice is needed to navigate this issue and some exceptions will apply. The move to a zero PPF levy this year and removing the PPF admin levy are positive steps. However, the PPF levy is not guaranteed to be zero in future.

Why it matters

Virgin Media issues have been causing headaches for accounting disclosures and risk settlement transactions since the ruling in 2023. The new changes largely help to resolve this issue, but do need to be worked through with the Trustee and Scheme Actuary.

The PPF’s funding position is in rude health. Removing high levy payments and the admin around them is positive for sponsors and trustees and gives a P&L benefit for sponsors, although this does not mean the PPF levies are gone for good.

-

Looking forward to next quarter

- We will be hosting a breakfast event at the London Stock Exchange with David Smith as the guest speaker and an expert panel including DWP director Kerstin Parker on 17 November. This event is for senior finance leaders with responsibility for their organisation’s DB and DC schemes. Register here.

- On 18 November, we will be hosting our Fiduciary Management Conference Live event on Zoom. Learn more and register here.

- Keep an eye out for an email about our upcoming accounting webinar.

- The Chancellor is expected to announce her Autumn budget on Wednesday 26 November. The press has speculated on the inclusion of several pensions related topics. We will be listening carefully to the content on Budget day and will let you know any implications in the next edition of IQ.

Your opportunity to provide feedback on IQ

It has been one year since we launched IQ with the purpose of sharing a quarterly reflective analysis and forward look ahead. We would appreciate a couple of minutes of your time to complete this anonymous short survey to help us ensure we maximise the value of IQ for our readers.

Join our mailing list

Get the next issue of Isio Quarterly delivered straight to your inbox