Welcome to IQ

Welcome to Isio’s latest quarterly pensions update for sponsors, summarising key events from the quarter and looking ahead to what’s coming up.

Changes since 30 September 2025

Commentary over the quarter

- Gilt yields have decreased by c. 30 basis points.

- Inflation expectations have reduced slightly.

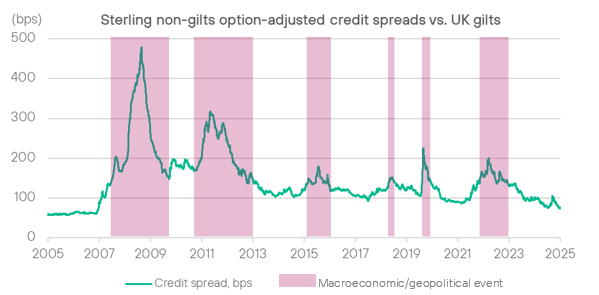

- Credit spreads have narrowed by c. 2 basis points at most durations, which we expect will have a negligible impact on accounting positions.

- Global equity markets were up by c. 3-4% over Q4 2025, but this wasn’t sufficient to fully offset the increase in liability values from reduced bond yields, so schemes with higher equity exposures may have seen their funding levels dip slightly.

- Insurer appetite continues to be strong going into the new year. The PRA has sent correspondence to insurers around the need to maintain pricing discipline and risk management standards, so we may see pricing harden, despite increased competition.

New year – new opportunities?

Background

Value across almost all traditional asset classes is hard to find, despite regular – often geopolitically induced – volatility. Many equity markets are at or close to all-time highs, and in most sectors credit spreads are at multi-decade lows, with both priced for perfection. Given this background, it can appear challenging for investors to identify compelling opportunities. This isn’t just a dilemma for growth-seeking portfolios. De-risking schemes face their own conundrum, with “safe” assets such as corporate bonds now carrying premium valuations. This could drive additional prudence into actuarial assumptions.

Isio’s view

Corporate bonds – often the bedrock of de-risking strategies, due to their interest rate sensitivity, cash flow generation and high credit quality – now present schemes with a risk. Spreads have contracted to levels that seemingly ignore default risk almost entirely. Rather than de-risking, allocating at today’s spreads could be seen as re-risking. The critical question isn’t whether to hold corporate bonds, but when. Schemes can replace static allocation targets with dynamic triggers to avoid the current value trap and in the interim consider alternative asset classes outside of traditional markets where there is still value to be had. ‘Capital Call Finance’ and ‘Private Investment Grade Credit’ are two such opportunities, with an allocation to these areas seeking to provide added diversification at attractive risk-adjusted yields, while maintaining an Investment Grade focus.

Why it matters

Scheme funding has generally improved as rates have risen and growth assets have performed well. In an environment where it is challenging to identify good opportunities, there is a risk that this leads to inaction or inappropriate de-risking. Schemes are at risk of letting go of hard-won gains should credit spreads widen or equity markets fall.

November’s budget introduced two important changes for UK pension provision

Restrictions on salary sacrifice arrangements

The tax-efficient pension contributions employers and employees can make through salary sacrifice arrangements will be capped. Currently employers benefit from reduced National Insurance Contributions (NIC) by redirecting portions of salary into pensions, as sacrificed pay is exempt from employer NIC (15%). Under the new rules, which are due to come into effect in 2029, only the first £2,000 sacrificed annually qualifies for this relief increasing NIC for employers.

For an employee sacrificing £5,000 p.a. (basic rate taxpayer):

| Now | In 2029 | |

| Employer saving p.a. | £750 | £300 |

| Employee saving p.a. | £400 | £160 |

For a mid-sized firm with 100 employees utilising salary sacrifice above the threshold, this could mean an average annual cost increase of £45,000 depending on participation rates and salary levels.

Employers may face tough choices: absorb higher NIC costs, limit pension contributions to the cap (potentially affecting employee retention), or restructure benefits. Sectors with high earners or generous pension schemes will feel the greatest impact. Proactive communication and financial planning will be critical to mitigate disruption to workforce well-being and long-term savings strategies. There are wider considerations to address the full impact which is outlined within our Budget 2026 Salary Sacrifice Checklist.

Lump sum DB surplus payments to members

It is currently highly tax inefficient to make lump sum payments to defined benefit (“DB”) members who are already receiving a pension. New legislation will make lump sum payments to members over minimum pension age “authorised”, so that they are instead taxed at the individual’s marginal rate (where DB schemes are in surplus on a low dependency basis). This should be enacted before the new wider surplus regime comes into force in late 2027.

Whilst sponsors of schemes that are running on may typically expect to receive most or all the surplus, this change is helpful because member shares of surplus can be used more efficiently. This may make it easier for trustees to agree to a higher overall employer share of surplus. Employers may also prefer enhancements that do not build-up additional DB risk.

A new route for sponsors to exit DB pensions while unlocking surplus value

Background

In December, investment manager Aberdeen announced a deal to effectively step in as sponsor of Stagecoach’s £1.2bn DB pension scheme, which was in surplus.

Stagecoach gets a clean break from its pension liabilities, while releasing some existing surplus funds for itself and scheme members.

Aberdeen will run the scheme on with a view to generating further surplus that it will share with members, while also managing the scheme’s assets.

Isio’s view

This solution will be of interest to those companies keen to be free of their UK DB pension exposure, with no desire to continue running the scheme for “profit” once it moves into surplus.

We are already seeing significant market interest. However, while Aberdeen is open to further deals, it has not clarified the scale of its ambition. Other similar asset management businesses may therefore see opportunities to develop similar offerings.

The structure will need scheme trustees who are willing to accept a move to a different sponsoring business and to forego any near-term opportunity to insure their members’ benefits. Realistically, not all will be of this view, despite the potential for members’ benefits to be enhanced in future.

Why it matters

For the right situations, this solution offers companies an attractive new option for removing their pension risks.

While the Stagecoach scheme was in surplus, we expect that transactions could be completed at no cost for those schemes not quite able to afford full insurance at present.

Furthermore, the scheme can potentially be passed to Aberdeen much more quickly than transferring it away under an insurance transaction – attractive in M&A situations especially.

Where’s your bank interest going?

Background

One of the most important functions of a Scheme Administrator is managing the trustee bank account on behalf of the trustee, and making sure there are sufficient funds to pay members’ benefits and scheme expenses.

Whilst it is the scheme’s money in these accounts, it is not uncommon for the interest on the money held in those accounts to be claimed – in part or completely – by the administrator.

Isio’s view

We believe all interest earned on the scheme’s money belongs to the trustee, and that’s the approach we apply on all of our administration appointments.

It has become clear that a number of administrators in the market retain the interest. This adds an additional cost to the administration services. What’s more, this isn’t always made clear when reviewing administration costs.

Why it matters

Whilst interest rates were low, this wasn’t too much of a concern. However, with interest rates now higher, this cost has increased – and can be more than the annual administration fee in some cases.

Trustees and sponsors should be clear on what happens to the interest currently, and factor it into decisions on administration reviews to ensure that overall costs remain in line with the market. It may be possible to re-negotiate the approach or even seek a refund of historic interest.

Cash flow management policies should also be reviewed where interest is currently not paid to the scheme, to ensure surplus funds aren’t left in the bank account.

If you’d like any support in considering your scheme administration, please contact jonathan.summerlin@isio.com

Market consolidation, regulatory momentum and the rise of CDC signal a turning point for DC pensions

Background

December saw a flurry of change within the DC pension provider market, with more expected.

This included:

- WTW acquiring NatWest Cushon master trust;

- Smart Pension completing the Options Workplace Pension Trust consolidation;

- Aegon announcing a strategic review and potential sale of Aegon UK;

- The unconnected multiple employer Collective Defined Contribution (CDC) regulations being finalised;

- TPR publishing their draft updated CDC Code of Practice; and,

- The Government’s consultation on Retirement CDC schemes closing.

Isio’s view

The Government’s continued push for consolidation is bearing fruit. These announcements are not a surprise given the number of ‘small’ providers in the market, and the Pension Schemes Bill 2025 unveiling a £25bn AUM scale requirement by 2030. We expect providers with assets below £15bn to now be reviewing their options, with further consolidation being inevitable.

The final hurdles for making unconnected multiple employer CDC schemes are now in sight. TPR is on track to accept applications for authorisation from mid–2026. The first schemes could launch from early 2027.

Why it matters

Businesses choose the provider that best meets their needs and objectives. Consolidation may impact their ability to meet those objectives, and unique selling points can be lost. Provider reviews should look at meeting current needs, with a level of future-proofing – making sure any known future changes are satisfactory.

Multi-employer CDC schemes will allow employers and their staff to access the benefits of CDC – higher stable incomes with no investment decision making for members – using a scheme established by a third-party provider (similar to using an existing DC Master Trust).

Looking forward to next quarter

- The next version of the CMI longevity projection model is due to be issued in March 2025. This update is expected to be a ‘business as usual’ approach and the CMI do not intend to consult on any changes.

- Take a look at our 2026 investment themes paper.

- Clara have been working on their offering for smaller schemes, which will be rolled out on a selective basis over the coming months to develop the solution.

- Watch out for the release of the results of Isio’s Independent Pension Trustee survey.

-

Changes since 30 September 2025

Commentary over the quarter

- Gilt yields have decreased by c. 30 basis points.

- Inflation expectations have reduced slightly.

- Credit spreads have narrowed by c. 2 basis points at most durations, which we expect will have a negligible impact on accounting positions.

- Global equity markets were up by c. 3-4% over Q4 2025, but this wasn’t sufficient to fully offset the increase in liability values from reduced bond yields, so schemes with higher equity exposures may have seen their funding levels dip slightly.

- Insurer appetite continues to be strong going into the new year. The PRA has sent correspondence to insurers around the need to maintain pricing discipline and risk management standards, so we may see pricing harden, despite increased competition.

-

New year – new opportunities?

Background

Value across almost all traditional asset classes is hard to find, despite regular – often geopolitically induced – volatility. Many equity markets are at or close to all-time highs, and in most sectors credit spreads are at multi-decade lows, with both priced for perfection. Given this background, it can appear challenging for investors to identify compelling opportunities. This isn’t just a dilemma for growth-seeking portfolios. De-risking schemes face their own conundrum, with “safe” assets such as corporate bonds now carrying premium valuations. This could drive additional prudence into actuarial assumptions.Isio’s view

Corporate bonds – often the bedrock of de-risking strategies, due to their interest rate sensitivity, cash flow generation and high credit quality – now present schemes with a risk. Spreads have contracted to levels that seemingly ignore default risk almost entirely. Rather than de-risking, allocating at today’s spreads could be seen as re-risking. The critical question isn’t whether to hold corporate bonds, but when. Schemes can replace static allocation targets with dynamic triggers to avoid the current value trap and in the interim consider alternative asset classes outside of traditional markets where there is still value to be had. ‘Capital Call Finance’ and ‘Private Investment Grade Credit’ are two such opportunities, with an allocation to these areas seeking to provide added diversification at attractive risk-adjusted yields, while maintaining an Investment Grade focus.

Why it matters

Scheme funding has generally improved as rates have risen and growth assets have performed well. In an environment where it is challenging to identify good opportunities, there is a risk that this leads to inaction or inappropriate de-risking. Schemes are at risk of letting go of hard-won gains should credit spreads widen or equity markets fall. -

November’s budget introduced two important changes for UK pension provision

Restrictions on salary sacrifice arrangements

The tax-efficient pension contributions employers and employees can make through salary sacrifice arrangements will be capped. Currently employers benefit from reduced National Insurance Contributions (NIC) by redirecting portions of salary into pensions, as sacrificed pay is exempt from employer NIC (15%). Under the new rules, which are due to come into effect in 2029, only the first £2,000 sacrificed annually qualifies for this relief increasing NIC for employers.

For an employee sacrificing £5,000 p.a. (basic rate taxpayer):

Now In 2029 Employer saving p.a. £750 £300 Employee saving p.a. £400 £160 For a mid-sized firm with 100 employees utilising salary sacrifice above the threshold, this could mean an average annual cost increase of £45,000 depending on participation rates and salary levels.

Employers may face tough choices: absorb higher NIC costs, limit pension contributions to the cap (potentially affecting employee retention), or restructure benefits. Sectors with high earners or generous pension schemes will feel the greatest impact. Proactive communication and financial planning will be critical to mitigate disruption to workforce well-being and long-term savings strategies. There are wider considerations to address the full impact which is outlined within our Budget 2026 Salary Sacrifice Checklist.

Lump sum DB surplus payments to members

It is currently highly tax inefficient to make lump sum payments to defined benefit (“DB”) members who are already receiving a pension. New legislation will make lump sum payments to members over minimum pension age “authorised”, so that they are instead taxed at the individual’s marginal rate (where DB schemes are in surplus on a low dependency basis). This should be enacted before the new wider surplus regime comes into force in late 2027.

Whilst sponsors of schemes that are running on may typically expect to receive most or all the surplus, this change is helpful because member shares of surplus can be used more efficiently. This may make it easier for trustees to agree to a higher overall employer share of surplus. Employers may also prefer enhancements that do not build-up additional DB risk.

-

A new route for sponsors to exit DB pensions while unlocking surplus value

Background

In December, investment manager Aberdeen announced a deal to effectively step in as sponsor of Stagecoach’s £1.2bn DB pension scheme, which was in surplus.

Stagecoach gets a clean break from its pension liabilities, while releasing some existing surplus funds for itself and scheme members.

Aberdeen will run the scheme on with a view to generating further surplus that it will share with members, while also managing the scheme’s assets.

Isio’s view

This solution will be of interest to those companies keen to be free of their UK DB pension exposure, with no desire to continue running the scheme for “profit” once it moves into surplus.

We are already seeing significant market interest. However, while Aberdeen is open to further deals, it has not clarified the scale of its ambition. Other similar asset management businesses may therefore see opportunities to develop similar offerings.

The structure will need scheme trustees who are willing to accept a move to a different sponsoring business and to forego any near-term opportunity to insure their members’ benefits. Realistically, not all will be of this view, despite the potential for members’ benefits to be enhanced in future.

Why it matters

For the right situations, this solution offers companies an attractive new option for removing their pension risks.

While the Stagecoach scheme was in surplus, we expect that transactions could be completed at no cost for those schemes not quite able to afford full insurance at present.

Furthermore, the scheme can potentially be passed to Aberdeen much more quickly than transferring it away under an insurance transaction – attractive in M&A situations especially.

-

Where’s your bank interest going?

Background

One of the most important functions of a Scheme Administrator is managing the trustee bank account on behalf of the trustee, and making sure there are sufficient funds to pay members’ benefits and scheme expenses.

Whilst it is the scheme’s money in these accounts, it is not uncommon for the interest on the money held in those accounts to be claimed – in part or completely – by the administrator.

Isio’s view

We believe all interest earned on the scheme’s money belongs to the trustee, and that’s the approach we apply on all of our administration appointments.

It has become clear that a number of administrators in the market retain the interest. This adds an additional cost to the administration services. What’s more, this isn’t always made clear when reviewing administration costs.

Why it matters

Whilst interest rates were low, this wasn’t too much of a concern. However, with interest rates now higher, this cost has increased – and can be more than the annual administration fee in some cases.

Trustees and sponsors should be clear on what happens to the interest currently, and factor it into decisions on administration reviews to ensure that overall costs remain in line with the market. It may be possible to re-negotiate the approach or even seek a refund of historic interest.

Cash flow management policies should also be reviewed where interest is currently not paid to the scheme, to ensure surplus funds aren’t left in the bank account.

If you’d like any support in considering your scheme administration, please contact jonathan.summerlin@isio.com

-

Market consolidation, regulatory momentum and the rise of CDC signal a turning point for DC pensions

Background

December saw a flurry of change within the DC pension provider market, with more expected.

This included:

- WTW acquiring NatWest Cushon master trust;

- Smart Pension completing the Options Workplace Pension Trust consolidation;

- Aegon announcing a strategic review and potential sale of Aegon UK;

- The unconnected multiple employer Collective Defined Contribution (CDC) regulations being finalised;

- TPR publishing their draft updated CDC Code of Practice; and,

- The Government’s consultation on Retirement CDC schemes closing.

Isio’s view

The Government’s continued push for consolidation is bearing fruit. These announcements are not a surprise given the number of ‘small’ providers in the market, and the Pension Schemes Bill 2025 unveiling a £25bn AUM scale requirement by 2030. We expect providers with assets below £15bn to now be reviewing their options, with further consolidation being inevitable.

The final hurdles for making unconnected multiple employer CDC schemes are now in sight. TPR is on track to accept applications for authorisation from mid–2026. The first schemes could launch from early 2027.

Why it matters

Businesses choose the provider that best meets their needs and objectives. Consolidation may impact their ability to meet those objectives, and unique selling points can be lost. Provider reviews should look at meeting current needs, with a level of future-proofing – making sure any known future changes are satisfactory.

Multi-employer CDC schemes will allow employers and their staff to access the benefits of CDC – higher stable incomes with no investment decision making for members – using a scheme established by a third-party provider (similar to using an existing DC Master Trust).

-

Looking forward to next quarter

- The next version of the CMI longevity projection model is due to be issued in March 2025. This update is expected to be a ‘business as usual’ approach and the CMI do not intend to consult on any changes.

- Take a look at our 2026 investment themes paper.

- Clara have been working on their offering for smaller schemes, which will be rolled out on a selective basis over the coming months to develop the solution.

- Watch out for the release of the results of Isio’s Independent Pension Trustee survey.

Your opportunity to provide feedback on IQ

It has been one year since we launched IQ with the purpose of sharing a quarterly reflective analysis and forward look ahead. We would appreciate a couple of minutes of your time to complete this anonymous short survey to help us ensure we maximise the value of IQ for our readers.

Join our mailing list

Get the next issue of Isio Quarterly delivered straight to your inbox