US election result: what does this mean for markets and investors?

Investment

Donald Trump is now President-elect of the United States of America. The Republican Party has also won the Senate and (as of 13:30 GMT, 6th November) appear on track to win control of the House of Representatives too. What do the election results mean for markets and investors?

How did the results play out?

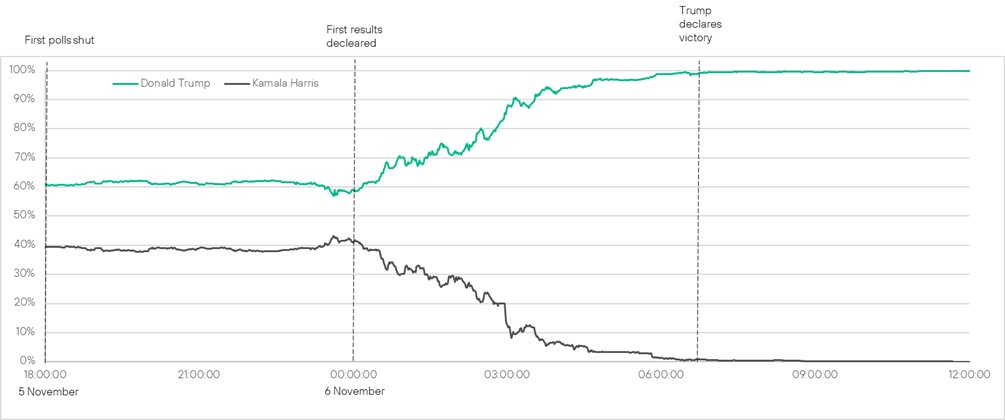

Many observers were expecting a drawn out results process, with the possibility that it would be days or even weeks before the final result was known. In the end though there were signs that Trump was performing well almost as soon as the polls closed, and key swing states all turned red shortly after: North Carolina was called at 4:40am GMT, Georgia at 5:37am and by the time Pennsylvania was called at 7:07am a Trump victory was all but assured.

Election victory odds

Market reaction

Markets reacted quickly to price in the consequences not only of a Trump presidency, but a full Republican sweep of the legislature too, meaning key policies would be easier to pass and not blocked or watered down by a Democrat controlled House or Senate.

Equities were buoyed by the prospect of corporate tax cuts and deregulation, whilst Treasury yields rose at the prospect of these inflationary policies and expectations of increased government borrowing. USD strengthened against other major currencies. Gilts and European Bond yields seem not to have been impacted by the result.

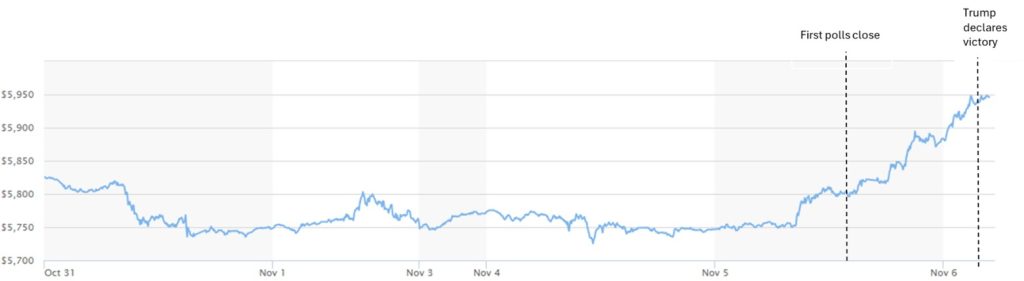

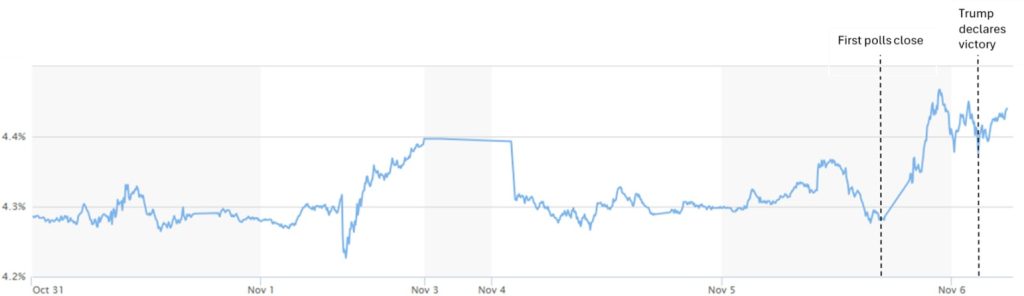

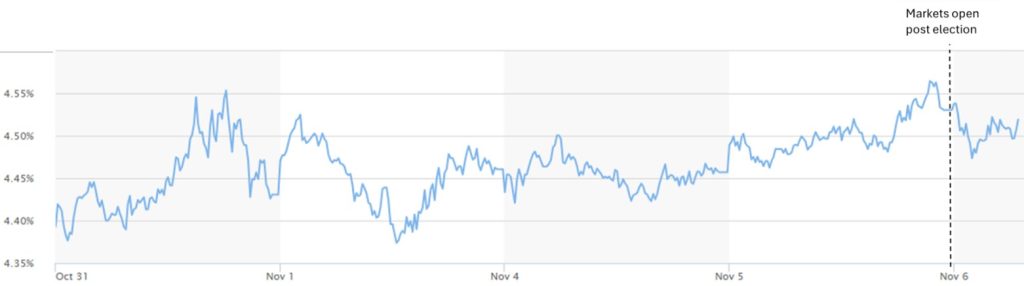

| Market | Change 00:00 GMT to 13:30 GMT |

| S&P500 (E-mini futures) | +2.15% |

| USD/GBP | +1.43% |

| 10 Year US Treasury Yield | +16.2 bps |

| 10 Year UK Gilt Yield | +1.9bps |

S&P500 (E-mini futures)

10 Year US Treasury Yields

10 Year UK Gilt Yields

Implications for investors

Looking forward, we will be monitoring three key areas:

- Whether Trump’s campaign rhetoric on tariffs, migration or taxes are actually converted into policy remains to be seen, however, a Republican legislature and friendly courts make it more likely. These actions would likely be inflationary and supportive of dollar strengthening – potentially disruptive to the Fed’s ‘soft landing’ in controlling a recent bout of inflation without entering recession.

- Trump can be erratic and prone to foreign policy brinkmanship. With active wars in Ukraine and the Middle East, as well as threats to Taiwan, this increases the risk of a diplomatic misstep leading to geopolitical conflict. Preparing for Black Swan events and out of model risks are more important than ever.

- This could impact sustainable investments opportunities. Trump is likely to repeal some of the more climate focused aspects of the Inflation Reduction Act, such as support for renewables, and create a hostile environment for ESG investment in the US. Managing climate risks and opportunities will continue to be important for investors and we will monitor knock-on impacts for the UK market

Conclusion

A Trump presidency, supported by a Republican House and Senate, will likely be good for corporate profits and therefore US equity markets in the short run. The US makes up c60% of the global equity market, but tariffs could be harmful to key emerging market economies like China and Mexico. In the bond market, there is a risk treasury yields will be penalized as a result of large scale borrowing and inflationary policies under the new regime – something we will monitor.

We are also aware that with Donald Trump, we should expect the unexpected. We encourage clients to make contingency plans to handle tail risks that appear more likely with Trump at the helm.

Barry Jones

Barry Jones