What does the new regime shift mean for credit investors?

Investment

Shifting from an ultra-low interest rate environment may be a welcome change for credit investors, but the transition from the previous regime is likely to be challenging.

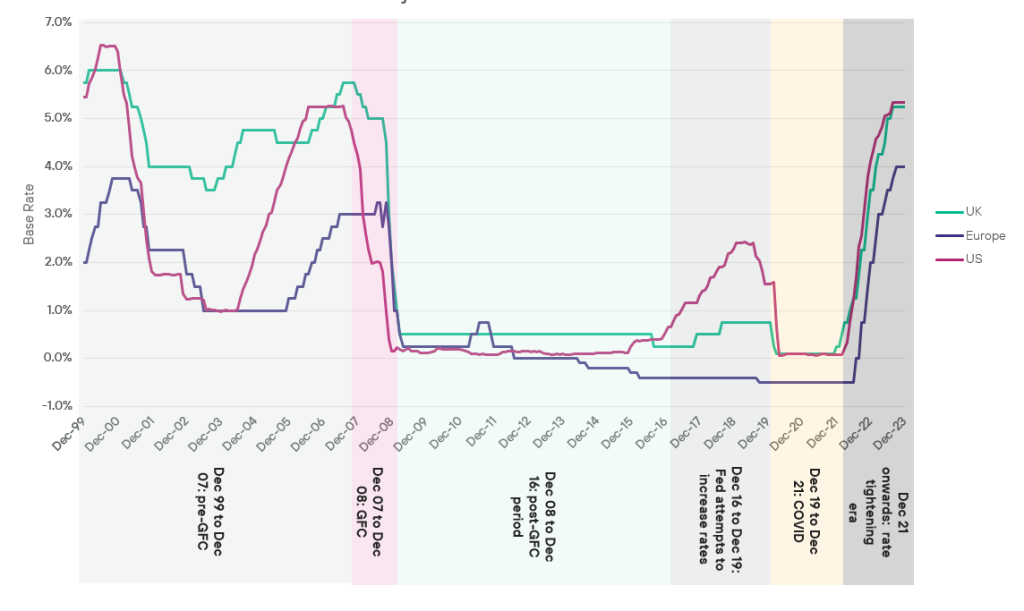

The idea of ‘normal market conditions’ is a fanciful concept that exists only in rudimentary economics textbooks. In any given environment, there are idiosyncrasies and dislocations that investors are searching for to both avoid being caught out and take advantage of. In recent years, for example, these have included government debt crises, geopolitical shocks, and the occasional country-splitting once-in-a-generation referendum (oh, and a global pandemic). Despite these departures from a steady state, following the global financial crisis (‘GFC’) markets settled on an established order whereby interest rates were low and central banks came to the rescue whenever economic shocks threatened to derail the global economy. Clearly, this era is now over as markets emerge from the longer-than-initially-advertised ‘post-GFC’ period of 2008-2022.

What did the previous era look like?

Arguably, the aforementioned post-GFC period was a greater departure from ‘normal’ market conditions than what we are now faced with. In a nutshell, the global economy was put on life support with rates slashed close to zero (even negative in Europe for seven years) with extensive quantitative easing programmes issued and extended whenever economies looked like they needed propping up. As above, this period was not without its external shocks, but given the safety net of loose monetary policy, investors were encouraged to take additional risk.

In credit markets, dislocation coming out of the crisis presented value for opportunistic investors, while loose monetary policy helped to keep defaults low across the board. However, in more recent years, low yields and spreads kept total returns more modest. A lack of market dispersion also reduced the opportunity set for active credit managers to demonstrate their value. As such, investors tended to utilise credit for de-risking purposes, rather than for attractive return generation.

What does the new era look like?

While many economic commentators warned of the unsustainability of the low interest rate period and desirability of rates moving closer to a long term equilibrium rate, it took significant inflationary pressures to convince central banks to finally increase interest rates. These pressures first presented themselves following the COVID liquidity injections and supply chain issues that were appearing amidst a general deglobalisation trend. While initially this inflation was dismissed as ‘transitory’, the outbreak of the Russia/Ukraine conflict acted as an unwanted catalyst to send global inflation soaring.

To many people (such as myself), low interest rates are all they had ever known, with global base rates only recently breaking out of a 15 year-long sub-5% period. For many more seasoned rates followers, the return to a higher rate regime is a desirable, long overdue occurrence. Higher rates should provide reward for savers, prevent asset bubbles, and give central banks room to cut if growth slows/inflation falls. While these are all fair points, the impacts of the 15-year ‘old regime’ mean the transition to this new era is likely to be challenging.

For instance, high availability of credit and low rates led to excessive amounts of debt being issued, with the IMF estimating that total global outstanding debt reached $307trn in 2023. This debt will need re-servicing at much higher interest rates, potentially having been secured against assets that have fallen in value. We have already seen initial signs of higher rates leading to parts of the economy cracking, with the US regional banking crisis and bail-in of Credit Suisse in March 2023 being alarming indications of this.

Moving forward, by design higher rates mean lower economic demand and therefore growth. Corporate profitability and balance sheets are likely to be impacted by this, especially smaller and more cyclical companies. While the bulk of upcoming leveraged loan maturities aren’t until 2025/262, the pressure on companies to re-finance early to manage liquidity concerns and potential credit ratings downgrades will effectively bring many of these forward into 2024, meaning these issuers are at the mercy of how rates and spreads move over the coming months.

Higher rates are also challenging for property markets, given the potential impact on underlying real estate prices. Commercial property has been suffering from long term structural headwinds for some time, particularly in retail, while the work-from-home trend has consigned many office assets to be considered weak collateral. Residential property, often underpinned by floating rate mortgages, is also likely to come under pressure, with c.£320bn worth of UK mortgage borrowers’ fixed rate periods due to expire by the end of 20243, which represented c.20% of the £1.6trn of UK mortgage debt outstanding in 20233. Any upcoming re-mortgaging will – you guessed it – be done at higher rates, eating into household disposable incomes. Higher rates also suppress new mortgage demand, impacting residential mortgage issuance and property prices negatively.

Where do interest rates go from here?

Just in case anybody didn’t appreciate the severity of the 2008 GFC, it says a lot that its impacts are still being felt in markets today and 15 years on we have only recently moved past the ultra-low rates era. Even this transition was forced by exogenous inflationary shocks forcing the hands of central banks, rather than policymakers voluntarily choosing to gradually increase rates. The Federal Reserve tried this over 2016-18 of course, but the market reaction encouraged them to backtrack even before COVID forced them to.

Where rates move from here is open to debate. While rates are likely to remain higher than 2008-22 moving forward, short term movements can be volatile and are likely to be very data dependent. Over Q4 2023, markets reacted to softening inflation figures and changing central bank rhetoric to swiftly price in optimistic rate cuts for 2024. While this has reversed slightly over 2024 so far, markets are still hopeful that rate cuts are forthcoming.

Moving forward, upcoming expected net gilt supply and quantitative tightening effects provide potential upward pressure on yields; conversely, any recession brought on by the above factors may force global central bankers to cut rates, particularly if inflation is under control and labour markets weaken. As the inverted gilt curve already reflects this scenario, any further fall in short term yields will require greater disinflation and/or a heavier recession than markets are already expecting.

What’s the upshot of this for credit investors?

Due to rising yields, 2022 was a painful year for fixed rate bond investors, a particularly bitter pill given many moved into these assets (such as investment grade corporate bonds) for their downside protection characteristics. Early last year, we published a paper outlining the attractiveness of credit spreads coming into 2023, which was borne out in practice, with bonds performing well and spreads tightening. All-in yields were supported by rising interest rates and look attractive even if spreads are now closer to longer term averages.

Moving forward, we expect interest rates to remain structurally higher and credit investors should readjust accordingly. Given the volatility of interest rates though, we do not advocate approaches reliant on duration and active interest rate calls to drive returns. We don’t wish to speculate on short term interest rates movements, instead, we are focused on identifying thematic trends that represent opportunities for credit investors.

For instance, within liquid credit, we expect fundamentals will be a greater driver of relative performance in the new environment, as opposed to loose monetary policy providing a supportive technical factor for all risk assets. We therefore expect to see greater dispersion both within and across different asset classes. As such, selecting a skilled value-focused manager to assess credit quality and identify opportunities is likely to be key, particularly in areas requiring a more active approach.

For less liquidity constrained investors, private credit looks attractive. Firstly, as higher interest rates have increased liquidity requirements for some investors, there is greater demand for a secondary market to offload performing private credit assets. As such, providing this liquidity presents an opportunity to access performing, mature illiquid credit assets at an attractive discount to fair value for those with the ability to do so.

Secondly, increased banking regulation following the regional banking issues of last year is constraining new bank lending and encouraging banks to offload existing exposures to tidy up their balance sheets. This is creating a wave of new opportunities within more bespoke strategies such as significant risk transfers (‘SRTs’ – providing regulatory capital relief to banks), NAV lending (loans to private equity funds, backed by their underlying portfolio) and non-performing loans (‘NPLs’ – taking non-performing assets such as commercial real estate debt from banks at a discount).

To summarise, whilst markets may be getting excited about the perceived prospect of rate cuts in 2024 – investors should prepare for the opportunities the new market environment might present.

Sources:

1 Bank of England; European Central Bank; Federal Reserve Board

2 S&P: Global Credit Markets Update | Q4 2023

3UK Finance, Morgan Stanley Research estimates