With change in occupational pensions accelerating, it’s simply not enough for the industry to keep pace.

The pensions industry needs to outpace change or risk falling behind and falling short of commitments to members, employees and the regulator.

That’s why we’ve launched ‘Outpacing Change’. We believe a more effective UK pensions system can only be achieved through new, bolder thinking across technology, funding, investments and more. Outpacing Change forms part of our commitment to share innovation that’s making a difference. tangibly improving outcomes for our clients – and our industry.

You’ll find the first in a series of solutions that are helping outpace change for you to download below.

Purposeful Run On: Unlocking further value in DB pensions

How can DB pensions work harder for members? Aggregate surplus across the UK’s c.5,000 private sector DB schemes is estimated at £250 billion. Isio is pioneering an exciting alternative destination for schemes which we call Purposeful Run On (PRO) – investing beyond full funding on a buy-out basis to share surpluses between members and sponsors gradually over the medium to long-term.

Isio Director, Matt Brown, introduces Purposeful Run On

PRO explained…

PRO is an exciting new long-term destination for DB Schemes. At its heart PRO recognises that in the right circumstances there may be a better way for scheme members and employers to benefit from reaching very strong funding positions.

Importantly, PRO can be implemented now for many schemes. The Government is consulting on introducing overriding legislation that would make this even easier. Government is also keen to change mindset about how sponsors and trustees think about future options for DB schemes. For many schemes PRO can be implemented now but for some it may be preferable to wait for overriding legislation to make refunding surplus possible irrespective of scheme rules. However, adopting PRO does require a change of mindset.

The funding level is tested each year and if the surplus on a buy-out basis exceeds an agreed buffer, surplus is immediately distributed. For example, if the buffer is set at 3%, and an annual test shows an estimated buy-out funding level of 105% then the value of the surplus distributed across members and the sponsor would be 2% of buy-out liabilities.

Members may receive their share through a discretionary pension increase or, potentially a lump sum (if the Government proceeds with consultation proposals) and sponsors through a refund. In the example above, if the surplus were shared evenly members would receive a 1% discretionary increase (or potentially a lump sum of equivalent value) and 1% of buy-out liabilities would be refunded to the sponsor in that year.

The PRO framework is not prescriptive. However, in our view there are two key principles:

1. There needs to be a meaningful share for both members and sponsors that incentivises both trustees and sponsor to agree to run on over the medium to long term after buy-out is first affordable.

2. Surplus needs to be shared gradually. This avoids inequalities between different generations of Scheme members and gives the sponsor confidence that it will receive a fair share of the surplus rather than relying on trustees applying discretions on wind-up many years into the future.

Trustees and sponsors of very well funded schemes expecting to buy-out in the near term have understandably focused on managing short-term downside risks. The expectation of investing over the long-term and meaningful upside for members and sponsors requires a different perspective, and will typically lead to higher return targets.

Typically, we’d expect a long-term target return of around gilts +1.5-2.0% pa. Schemes can use their greater flexibility and regulatory advantage over insurers to invest in a wider range of assets diversifying risks.

The long-term average improvement in funding position is expected to be 2.0-2.5% of assets per year. Of this, 0.5-1.0% comes from maturing and members exercising options – this can be achieved with a high degree of confidence. The remainder arises from higher expected investment returns (net of running expenses) than the discount rates implicit in insurer pricing bases.

Our stochastic modelling shows that after 10 years of running on, a typical PRO approach gives better outcomes for members and sponsors than insuring at the earliest opportunity in over 95% of scenarios. In the median case a typical scheme gradually releases 17% of initial assets over the first 10 years (shared between members and sponsor).

Pensions Age Q&A – Matt Brown sits down with Pensions Age Editor, Laura Blows to discuss PRO

Government consultation on options for DB schemes

On Friday 23rd February 2024, the Government launched its consultation on options for DB schemes that it trailed in the Autumn Statement. This includes proposed reforms to make it easier to use surpluses in well-funded schemes to make payments to employers and scheme members. If implemented this would be the most important change for UK DB schemes in over 20 years.

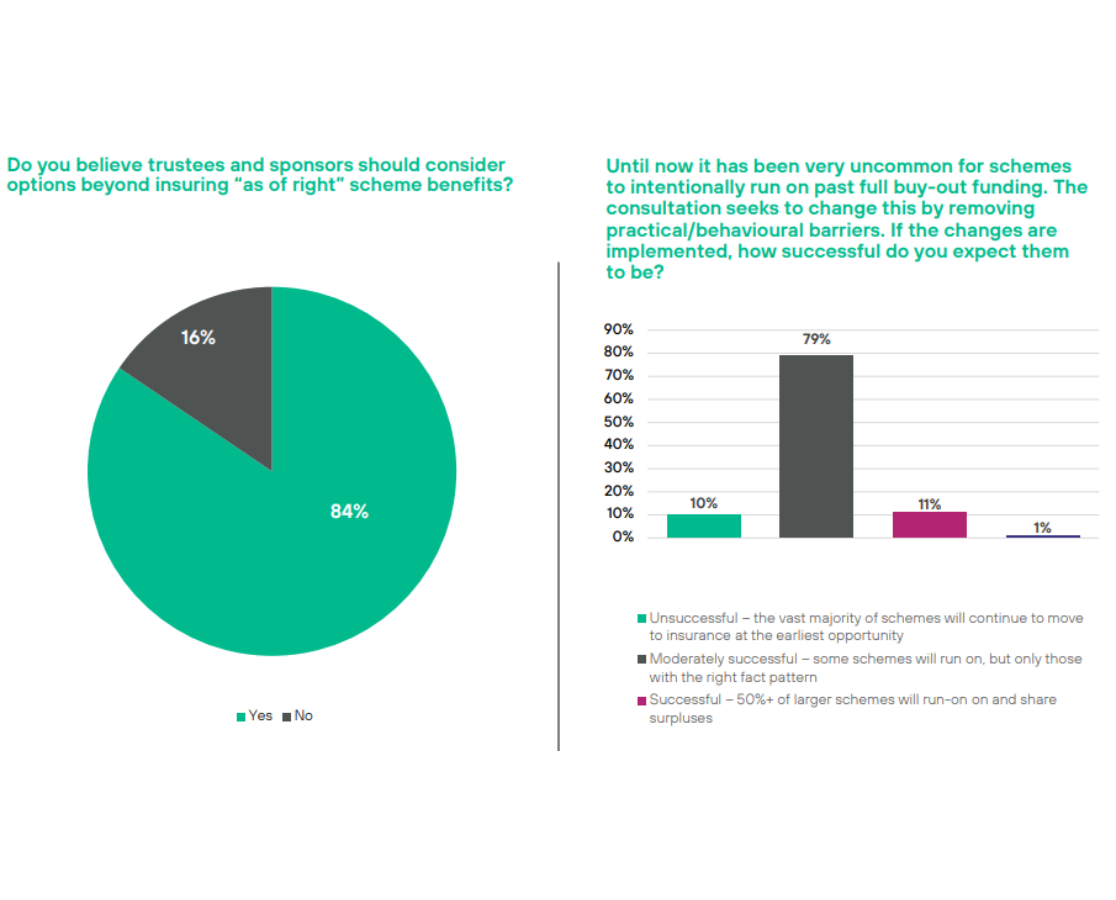

During our recent webinar, we polled an audience of pension professionals and you can see the results here.

Is a pensions revolution on the cards?

With DB schemes being better funded than ever before and being required to articulate their long term plans, more and more trustees and scheme sponsors are interested in run-on options.

The launch of the Government’s recent consultation which aims to make it easier to distribute surplus assets has turbo-charged levels of interest.

During our recent webinar, we heard the trustee and employer perspectives on the consultation and how it could enable better outcomes for members and sponsors of many schemes. Watch the highlights here. If you’d like to watch the full session, complete the form below.

Start a conversation

To learn more about how PRO could release additional value for members and sponsors, get in touch.

Matt Brown

Matt Brown

Director

Stewart Hastie

Stewart Hastie

Partner

Barry Jones

Barry Jones

Chief Investment Officer