Have stewardship or divestment been entirely effective to date?

Pensions

“It is our duty to protect God’s creation, and energy companies have a special responsibility to help us achieve the just transition to the low carbon economy we need.”

– The Most Revd Justin Welby, Archbishop of Canterbury, and Chair of the Church Commissioners for England.

The Church of England Pensions Board and Church Commissioners recently decided to disinvest from oil and gas majors.[i] This comes after prolonged engagements culminating in the pension funds noting a clear misalignment between the long-term interests of the funds’ members and oil and gas majors’ short-term profit maximisation.

In a previous blog, we covered the fact that as governments and oil and gas majors promote and confound decarbonisation efforts, a hotpot of climate activism is bridging the accountability gap. Investors are not immune, as shareholder activism and disinvestment are gaining traction.

As investors increase their focus on climate risks and opportunities, one common debate is around the effectiveness of divestment versus engagement with polluters to initiate change. In this blog, we have undertaken a review of industry literature to unpick this conundrum.

Blanket divestment is the exclusion of an entire sector, on sustainable investment grounds.

Whereas disinvestment is the selective exclusion of specific companies or assets.

Engagement is a purposeful, targeted communication with an entity (e.g. company or government) with the goal of encouraging change. Whether at the individual issuer level, or to address a market-wide system risk, such as climate change.

Divestment versus engagement as tools for climate action

Whilst the Church pension schemes’ disinvestment focuses on selective exclusion of laggards, divestment is the blanket exclusion of all companies in a sector – in this case, fossil fuels. When considering divestment, the specific revenue threshold used becomes important, for example, excluding all companies with at least 5% of revenues from fossil fuel-based activities results in very different portfolio outcomes versus say a 25% threshold. The leniency will determine how much energy and transport exposure remains.

After a look at the industry literature, to date, it is not necessarily possible to state that either engagement or divestment have been entirely effective in tackling the climate emergency. Many fossil fuel companies continue to drag in their transition efforts, and we remain off track for Paris. (Albeit there are exceptions, such as Ørsted, which has transformed from a fossil fuel company into a low carbon company, although it is not clear divestment or engagement forces had a role, as opposed to internal ambition.)[ii]

One significant challenge is disentangling the data on cause and effect. It is difficult to isolate causality in engagements influencing climate action. Albeit we have seen positive momentum, including under Climate Action 100+, this is compounded by other influences, such as consumer norms and decarbonisation regulation. Meanwhile divestment can create perverse incentives, in stifling capital to fossil fuel companies, causing rising fossil fuel prices, stronger returns for investors, and attracting more capital.[iii] Exiting from a company would also result in reduced ability to influence change,[iv] and may leave capital in the hands of less climate conscious investors.[v]

Escalating action to combat the climate

The key issue when looking at the literature is that there is no simple solution to get us back on track, but there are some common themes (summarised below):

Collective engagement is needed to ensure sufficient influence is exerted for companies to be compelled towards change.[vi] Government stewardship regulations are encouraging each individual pension scheme to set their own stewardship priorities and act, possibly in different directions.[vii] Working collectively will however be essential to ensure enough capital is pressured into decarbonisation.

Engagement escalation through to the threat of disinvestment is also important, to ensure a backstop where companies are failing to respond.[viii] (Some however argue this simply results in companies waiting investors out.[ix]) The key point is singling out the individual laggards to point the finger at, much like the Church pension schemes. Rather than generically pointing the figure at all energy and transport companies, some of which might be important in a future sustainable economy (albeit others not, where those companies fail to transition).

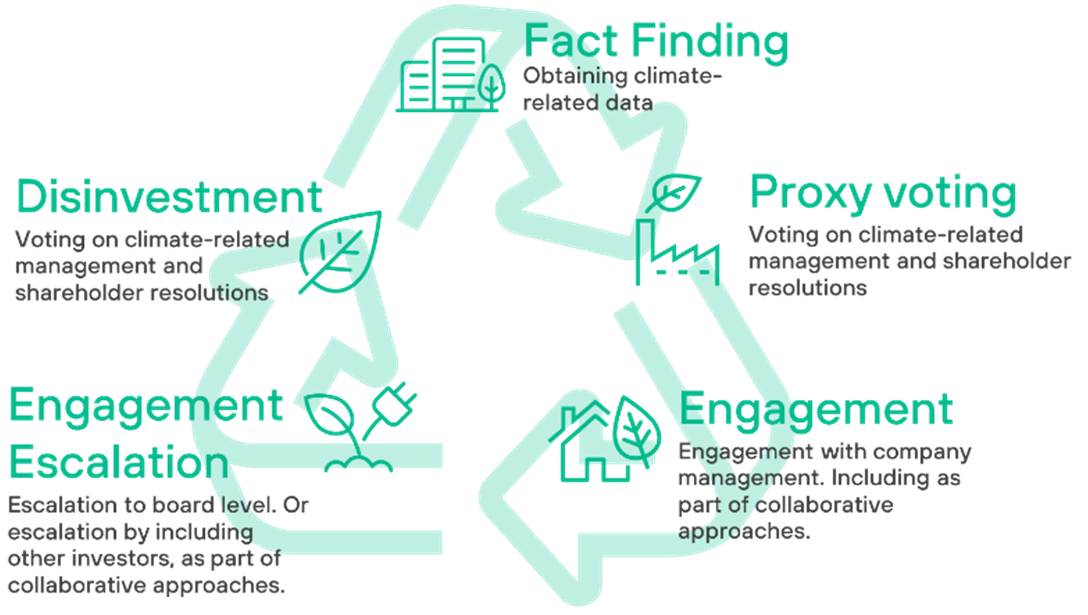

A circular approach. The very essence of the low carbon transition is that companies are, or should be, in flux. Any approach should recognise that companies may transition in-and-out of thresholds for engagement or disinvestment, over time, and the investor approach should respond accordingly (see chart).

When looking at focus areas to target climate action, attention could also be warranted on specific areas, with the literature pointing us to the below, in particular:

- Thermal coal, as the most emissions intensive fossil fuel, may carry a greater risk of asset stranding, [x] and therefore may also be associated with a higher near-term risk of degraded returns or defaults;

- Tackling fossil fuels debt, to recognise the dominance of debt in fossil fuel markets,[xi] and the fact that shareholder activism in equity markets is vital, but not the whole picture;

- Tackling new and additional financing (e.g. venture capital and private equity) actively contributing to the expansion of high carbon assets,[xii] particularly anything focused on new exploration and production; and,

- Recognising the significant role of government-owned enterprises (who own over half of fossil fuel reserves)[xiii] and banks (significant investors in the fossil fuel industry) in the climate crisis,[xiv] beyond the leading role oil and gas majors.

Next step considerations

Ultimately, investments will necessarily need to align with the best interests of beneficiaries. To determine what is in the beneficiary’s best interest, the first step could be to set out the climate outcome deemed the most likely, today, and align investments with that outcome. For example, where you believe a below 2⁰C scenario is most likely, ensuring portfolio mandates target that outcome explicitly should be a focus.

Beyond this, it could be prudent to “hedge your bets” against the plethora of possible climate futures with a comprehensive risk management approach to managing transition and physical risks. Today, we honestly don’t know what the climate future holds, other than the window to meeting 1.5⁰C this decade is rapidly closing, with some investors deeming this outcome less likely (outside the significant deployment of negative emissions technologies and nature-based investments). Physical risks could also be significant, particularly in light of climate action failure, which we covered in an earlier blog. Other considerations include:

- Agreeing and formalising a bespoke engagement policy, including setting out clear engagement escalation approaches to improve traction (e.g. considering the threat of disinvestment at a defined point of decarbonisation stalemate, or after a defined period of time);

- Ensuring managers have the climate capabilities to reflect your views;

- Assessing climate analytics (e.g. climate metrics and modelling) to identify company or asset class laggards in the portfolio, with a focus on those with the highest risk of asset stranding; and,

- Understanding portfolio trade-offs, for example, in bringing about significant decarbonisation, there may be social implications, with high carbon job losses generating a social cost.

Renewed action is needed to tackle the climate emergency and the individual investor response will necessarily be influenced by individual views on what is the right response. Agreeing climate objectives and central views are therefore the first step and something we regularly discuss with our clients. Regardless of the climate approach adopted, as we teeter on the brink of climate disaster, the time to act is now.

[i] Church Commissioners statement. Church Commissioners for England to exclude oil and gas companies over failure to align with climate goals | The Church of England

Church of England Pensions Board Statement. Church of England Pensions Board disinvests from Shell and remaining oil and gas holdings | The Church of England

[ii] Our Green Energy Transformation | Ørsted (orsted.co.uk)

[iii] Carlyle. (2022) Global Insights: Energy Transition. Carlyle_Global_Insights_Energy_Transition_Jason_Thomas_May_25_2022.pdf

[iv] Broccardo, E., Hart, O. and Zingales, L. (2020) Exit vs Voice. exit_vs_voice_1230 (harvard.edu)

[v] James, C. (2022) Don’t Sell Your Fossil-Fuel Stock If You Want to Make a Climate-Change Difference in 2022. Don’t Sell Your Fossil-Fuel Stock If You Want to Make a Climate-Change Difference in 2022 | TIME

[vi] For example: The Investor Forum. (2019) Collective Engagement: An essential stewardship capability. The-case-for-collective-engagement-211119.pdf (investorforum.org.uk)

And: PRI. (2013) Getting Started with Collaborative Engagement: How Institutional Investors Can Effectively Collaborate in Dialogue with Companies. download (unpri.org)

[viii] PRI. (2013) Getting Started with Collaborative Engagement: How Institutional Investors Can Effectively Collaborate in Dialogue with Companies. download (unpri.org)

[ix] Principles for Responsible Investment (PRI). (2022) Discussing divestment: Developing an approach when pursuing sustainability outcomes in listed equity. download (unpri.org)

[x] International Energy Agency (IEA) (2021) Net Zero by 2050. Net Zero by 2050 – Analysis – IEA

[xi] Quigley, E and Davies, S. (2021) Stock picking for humanity. Here are responsible shareholder tactics that actually work | Aeon Essays

[xii] Quigley, E and Davies, S. (2021) Stock picking for humanity. Here are responsible shareholder tactics that actually work | Aeon Essays

[xiii] IEA. (2020). The oil and gas industry in energy transitions. The Oil and Gas Industry in Energy Transitions – Analysis – IEA

[xiv] Quigley, E. and Davies, S. (2021) Stock-picking for humanity. Here are responsible shareholder tactics that actually work | Aeon Essays

Get in touch

Talk to us today to see how our bolder thinking can get you better results.