Recent market volatility – An update from our CIO

Pensions

The past few days have seen some large movements in markets, particularly in equities, triggered by the US jobs report on Friday.

Background – what has happened?

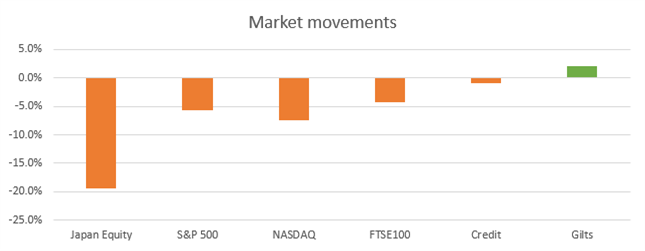

On Friday, the release of the monthly US jobs report showed US unemployment was rising and hiring was falling, both by much more than had been anticipated, prompting market commentary of an impending US recession. In response markets reacted quickly and severely (as shown in the table below), most notably:

- In the US, government bond yields fell (and prices increased) as market moved from pricing in 1-2 interest rate cuts this year by the Fed to 5 cuts;

- Equity markets sold off sharply across the world, particularly in Japan where they fell over 12% on Monday, meaning the worst 3-day crash for its market since 1973 (though some of this has been recovered today);

- Credit spreads widened, reflecting the concerns around slowing global growth, though movements were much more muted compared with what has been seen in equity markets;

- Oil and gold also both fell in value, with the latter failing to live up to its “safe haven” label.

It’s worth putting these moves into context. Before August markets were, broadly speaking, “pricing in perfection”, by which we mean:

- Investment grade credit spreads were extremely tight – below the 5th percentile of their historic trading ranges;

- Equity valuations were high – with “Equity Price to Earnings” ratios in similar statistical bands, especially in certain sectors.

Therefore a fall back in equities at some point felt inevitable but if we consider the market movements in the context of the large market gains made post-COVID, they are microscopic. It is also worth bearing in mind that this is August, a period where the investment markets operate on very thin volumes so smaller trades have a bigger impact and most investment desk heads are not in-situ.

Why did this occur?

Whilst the release of Friday’s jobs report was seemingly the catalyst for the significant movements of the past few days, it’s difficult to pinpoint the movements on any single event, but a number of reasons have been cited including:

- The weak jobs report challenging the previous view of a “soft landing” for global growth and that a recession can no longer be completely discounted. That said, government bond yields had already been moving lower in the past few weeks, already signalling a potential view of slower global economic growth (in the UK, government bond yields are down c0.4-0.5% since the end of June).

- Related to this, concerns that the US Federal Reserve is “behind the curve” and will need to cut interest rates sharply (and quicker than previously anticipated) in response to weaker growth and lower inflation;

- A shift in Japanese policy, with the Bank of Japan continuing to intervene in currency markets to support the Yen over July and raising base rates to 0.25% (from 0-0.1%) last week, the highest level since 2008. This undermines the Yen carry trade (where investors borrow in the lower yielding Yen to invest in higher yielding assets elsewhere);

- A shift in equity momentum away from big US tech stocks, which make up a substantial share of US and global equity markets, with concerns the sector won’t live up to its earnings expectations.

What do the recent market movements mean for UK DB schemes?

For a well hedged UK DB scheme with a modest allocation to higher risk assets such as equities, these movements will have been relatively muted, particularly compared to the 2022 sell-off which saw both equities and bonds sell-off sharply. The movements of the past few days / weeks are more representative of a sell-off driven by concerns around slowing economic growth, with government bonds increasing in value whilst equities fall (though this does mean that the value placed on a UK pension scheme’s liabilities is expected to have increased recently).

Where schemes have a large equity allocation or relatively lower liability hedge, they will have seen more significant funding level volatility, though higher bond yields and strong equity markets year to date will have meant substantial funding gains are likely to have been seen over 2024.

Finally, for any schemes within an insurance price lock, be mindful of boundary conditions and any basis risk you are running. If you are further away and well positioned this volatility should have had little impact.

Actions to consider

In our view, whilst recent economic data has weakened and hence the “soft landing” narrative has been tested, we think that the magnitude of the market movements of the past few days is disproportionately large compared to the severity of the news flow.

That said, we recognise that more substantial and prolonged shifts in markets and increased volatility could occur, particularly if economic data continues to weaken and recessionary fears increase further. We therefore recommend clients speak with their usual Isio contact and consider the following where relevant:

- Review any recent agreed strategic changes (that haven’t yet been implemented) in light of this market volatility and potential funding level changes;

- Review upcoming asset transitions given potentially heightened transaction costs – we haven’t seen this yet but this could change;

- For schemes close to insurance or in a price lock, review boundary conditions and any risks being run versus insurance pricing;

- Continue to review investment grade credit allocations given very tight credit spreads – we have discussed this with a number of clients and continue to recommend this action;

- For those clients that have benefitted from lower interest rate hedges and / or high equity allocations, review these positions and look to lock-in gains where appropriate;

- Where equity portfolios made up a substantial part of a scheme’s portfolio, review their construction for any significant concentrations (e.g. US tech stocks).

Whilst it seems, at this stage, that geopolitics hasn’t played a large part of the recent volatility, but there are a number of events on the horizon that could change this. We continue to recommend that clients review their strategy for “out of model” risks, such as geopolitical risk, and the impact these could have on their schemes’ portfolios and funding positions.

Barry Jones

Barry Jones