The decline of Defined Benefit pensions in FTSE 100 companies

Pensions

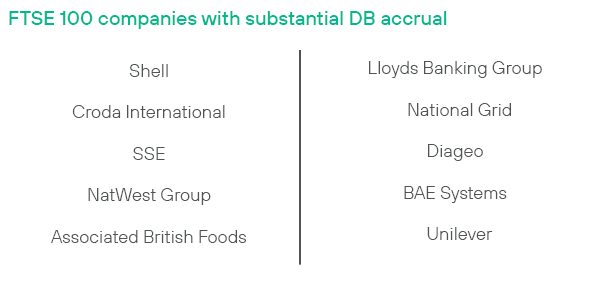

I recall being confidently told in 2012 that all UK defined benefit (‘DB’) schemes would be closed to future pension accrual by 2016. Looking at some of our largest UK companies today, who make up the FTSE 100, around a quarter still offer DB pensions to at least some of their staff. But a closer look reveals that only 10% are still providing DB in any meaningful way, and only one offers a DB scheme to new joiners.

So, 10 years on from that clearly inaccurate prediction, when do I think all remaining private-sector DB schemes will be closed? If I was having to place a bet, I would be pretty sure that this will happen by 2030.

What has driven the closure of defined benefit schemes?

Half of FTSE100 DB schemes have closed over the last decade. The three main reasons for this have typically been:

- To reduce costs – some DB pension schemes cost in excess of 20% of salaries (if not higher!)

- To reduce risk – many organisations have decided that very large DB pension schemes expose the business to the risk of significant deficits and wish to stop the liabilities growing

- To increase fairness – addressing the disparity in spend on employees in DB and defined contribution (‘DC’) arrangements

Will DB schemes continue to close?

It seems certain that the trends seen over recent years will continue. Albeit as the majority of large DB schemes are already closed the pace of change will inevitably slow.

In the current high inflation environment, we are seeing some companies facing increasingly significant pay claims. Against this backdrop, some will seek to make savings on their pensions spend, and at the same time address the pensions gap between DB and DC populations. However, we are also aware of companies putting pension change on the backburner to avoid potentially disrupting a post-pandemic recovery and tight labour market.

As most companies closed their schemes to new joiners more than 10 years ago, these schemes will naturally “self-close”. We envisage a rump of schemes will be left to run off over time in this way. For example, there are nine FTSE 100 companies where a cap on pensionable salary increases has been introduced. These limit the rate at which DB pensions can grow and provide cost savings for the company. But they can also make closing the schemes less likely, as to do so would introduce an unwelcome one-off cost as all benefits would automatically become linked to inflation in future.

So that’s it for defined benefits?

I can’t see many new DB schemes being created any time soon. When Royal Mail’s Collective Defined Contribution (“CDC”)scheme is launched later this year, it will herald a new era in benefit design innovation. I expect only a handful of employers to follow them in setting up their own CDC schemes. But, in the race for talent and to promote effective workforce management, many companies will have to review their long-term savings strategies. There is lots of potential for CDC mastertrusts, decumulation vehicles and better member engagement tools – but that’s for another blog!

Scott Kendrick

Scott Kendrick